Venture Corporation Ltd - Robust demand but shortages persist

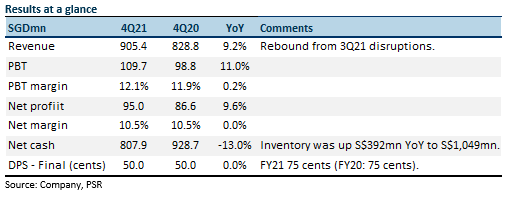

28 Feb 2022- Results met expectations. FY21 revenue and PATMI were 99% and 100% respectively of our estimates. 4Q21 revenue was up 9% YoY to S$905mn, recovering from a disrupted 3Q21. Final dividend of 50 cents unchanged from last year.

- Manufacturing returned to full capacity in Malaysia around September. But semiconductor shortages persisted in 4Q21.

- We raise FY22e PATMI by around 4%. The target price is also being increased to S$20.00 (previous S$19.20). The target price is based on 16x PE FY22e, its 5-year average. Our recommendation is an upgrade from NEUTRAL to ACCUMULATE. We expect stronger growth in FY22e. Order pipeline is healthy across all verticals but the availability of components will dictate the ability to fulfil demand. We believe Venture can better navigate these challenges with a record S$1bn build up in inventory and a higher readiness than in the past. The share price is supported by dividend yields of almost 5%, 13% ROEs and S$808mn net cash.

The Positive

+ Recovery in revenues. Revenue rebounded 9% YoY to S$905mn, just 3% shy of pre-pandemic levels. We believe some of the growth was driven by spill-over from prior quarter shutdowns in Malaysia. Growth was across all verticals.

The Negative

– Cash-flow generated lower due to inventory build-up. Free cash flow generated in FY21 was S$91mn, a sharp drop from FY20 S$425mn. Around $382mn of working capital has been deployed to build up inventory to cope with component shortages. FY21 capex was a record low of S$11mn. Net cash in the balance sheet stands at S$807.9mn (FY20: 928.7mn).

Outlook

Venture guided that demand is robust based on customer orders and forecast across all sectors. Notable strength is from analytical instruments, gene sequencing, instrumentation and lifestyle and wellness products.

Upgrade to ACCUMULATE from NEUTRAL with a higher TP of S$20.00

Our FY22e revenue is unchanged but PATMI is raised by 4%.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Trade of the Day - SATS Ltd (SGX: S58)

Trade of the Day - SATS Ltd (SGX: S58) Block Inc - Cost-cutting boost earnings

Block Inc - Cost-cutting boost earnings Trade of the Day - Oracle Corporation (NYSE: ORCL)

Trade of the Day - Oracle Corporation (NYSE: ORCL)