China Aviation Oil (Singapore) Corporation Ltd - Stock Analyst Research

| Target Price* | 1.050 |

| Recommendation | BUY› BUY |

| Market Cap* | - |

| Publication Date | 4 Mar 2024 |

*At the time of publication

China Aviation Oil - Net profit and dividend beat expectations

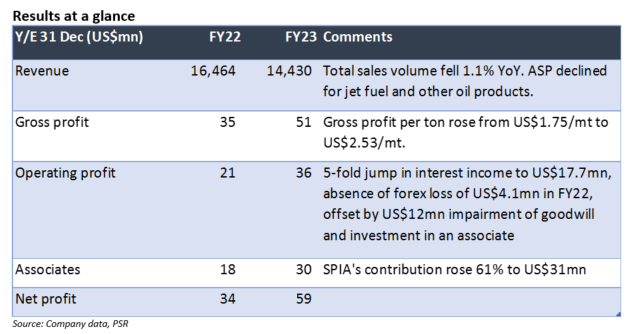

- The results beat our estimates by 22%, due to stronger-than-expected contributions from 33%-owned SPIA.

- Net profit rebounded 75.5% due to 1) stronger demand for jet fuel with borders reopened from early 2023; 2) higher margin per metric ton with increased direct sales with airline customers; and 3) SPIA’s net profit jumping 61% YoY. Net cash at year-end was US$373mn (S$0.623/sh). Full-year dividend was raised to 5.05 Sct (FY22: 1.6 Sct), a yield of 5.4%.

- China’s international air traffic is still at 37% below pre-Covid level. Flights are progressively being restored with further normalization of aviation services. China accounted for 62% of total revenue in FY23.

- Maintain BUY call and raised TP to DCF-derived TP to S$1.05 (prev. S$1.01). We lifted our FY24e net profit estimates by 17% to factor in improved gross margin.

The Positives

- Gross profit per metric ton jumped to US$2.53 in FY23 (FY22 US$1.75/mt). The margin in 2H23 was 145% higher YoY at US$3.78/mt. This was achieved through engaging in more end-to-end sales, sourcing products from refinery for delivery to the airline customers. This is compared to the typical low-margin back to back oil trading transaction. Higher volume also helps to lower unit fixed cost.

- Contributions from 33%-owned associate Shanghai Pudong International Airport Aviation Fuel Supply Co Ltd (SPIA) grew 61% to US$31mn. SPIA also paid US$23mn to CAO in FY23, 9.5% higher YoY. We expect a higher payout in FY24e after the strong FY23.

The Negative

- Provided for impairment of US$12mn for goodwill (US$3.4mn) and investment in an associate (US$8.7mn), thus lowering net profit.

About the author

Peggy Mak

Research Manager

PSR

Peggy has been a sell-side equity analyst for 22 years and a fund manager for 15 years.

About the author

Peggy Mak

Research Manager

PSR

Peggy has been a sell-side equity analyst for 22 years and a fund manager for 15 years.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU