HRnetGroup - Stock Analyst Research

| Target Price* | SGD 0.85 |

| Recommendation | BUY› BUY |

| Market Cap* | - |

| Publication Date | 26 Feb 2024 |

*At the time of publication

HRnetGroup Limited – Expecting growth to creep up

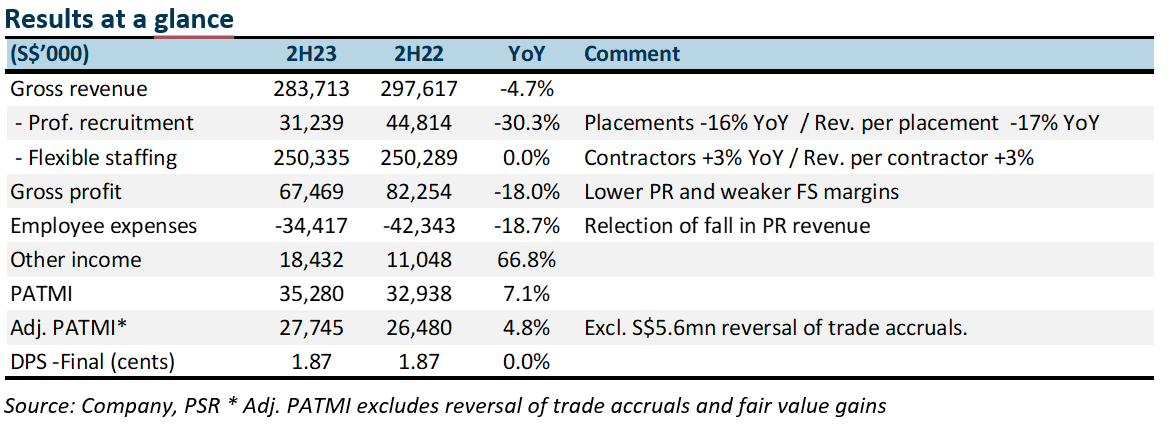

- Results were marginally below expectations. FY23 revenue and adjusted PATMI were 97%/95% of our forecast. 2H23 grew 5% YoY to S$27mn. Professional recruitment revenue was weaker than expected with a decline of 30% YoY. Placements were the lowest since listing.

- Flexible staffing remained resilient. Margins were softer with the absence of pandemic-related roles. Growth was from finance and manufacturing.

- Hiring in technology roles from start-ups to semiconductors has been a growth vertical for HRnet. However, the pace of hiring in this segment has slowed significantly. Growth will now come from capturing a larger share of customer budgets. HRnet office network and sphere of service including solutions in instant pay and claims, can raise the support of client needs in the region. Flexible staffing is benefiting from a rising wage environment, tight supply of local manpower and increased outsourcing. General hiring conditions are weak, particularly in China. We lowered our FY24e earnings by 11% to S$57mn. Our BUY recommendation is maintained. With the more tepid growth, we are reducing our valuation metric to 11x PE ex-cash FY24e (prev. 12x PE). Target price lowered from S$0.88 to S$0.85. It remains at a huge discount to global peers trading at an average PE of 19x.

The Positive

+ Flexible staffing (FS) is the key performer. Around 94% of FS revenue is from Singapore. 2H23 FS revenue in Singapore rose 1.8% YoY. Despite the decline in number of contractors, the rise in wages supported revenue. Government policy to drive up wages of the lower income also pushed income from government subsidies to S$6.6mn in 2H23 (2H22: S$1.2mn).

The Negative

– Professional recruitment (PR) is still the weak spot. The number of PR hirings in 2H23 fell 17% YoY to 2,856, due to hiring freezes and cautious sentiment. Revenue per placement declined 17% YoY as more placements were completed for junior roles.

Outlook

We are forecasting a 5% contraction in volumes for PR. There are limited indications corporates are ramping up their hiring of managerial roles in this region. FS revenue is expected to grow stronger from higher wages and improvement in volumes especially in Taiwan. The FS operations in Taiwan is beginning to hit scale and gain more traction with corporates.

Maintain BUY and lower TP of S$0.85 (prev. S$0.88).

HRnetGroup enjoys net cash of S$303mn with barriers of scale with more than 500 full-time recruitment consultants across 17 cities. There is another S14mn outstanding in their committed share buyback programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU