Netflix Inc – Re-acceleration in membership growth

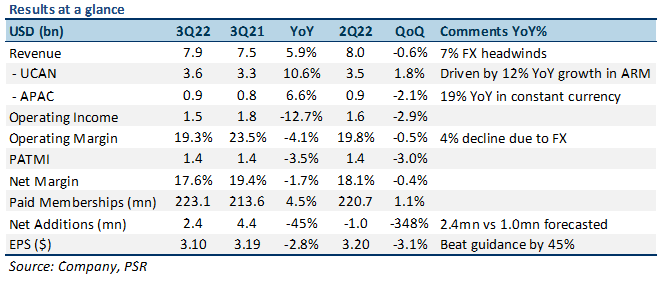

21 Oct 2022- 3Q22 revenue beat expectations even with 7% FX headwinds; earnings beat by 45%. 9M22 revenue/PATMI at 73%/82% of our FY22e forecasts. Earnings beat due to US$348mn EUR debt remeasurement and shift in spend from 3Q22 to 4Q22.

- Membership additions beat expectations (2.4mn actual vs 1mn expected). Initial demand from advertisers has been strong for the new ad-supported subscription plan.

- We maintain a BUY recommendation with a lowered DCF target price of US$346.00 (prev. US$399.00) as we lower FY22e revenue/PATMI forecasts by 3%/17% on the back of increasing FX headwinds, offset slightly by a raised terminal growth rate of 3% as we account for a longer-term improvement in revenue from advertising.

The Positives

+ Outperformance in membership additions. Netflix reported 2.4mn membership additions for 3Q22, 1.4mn more than it guided. APAC was the main driver of this, growing paid memberships 23% YoY, and contributing 1.4mn additions for the quarter. The outperformance of membership additions was a surprise given the high levels of inflation and a weaker macroeconomic environment. It also comes as a welcome relief after 2 consecutive quarters of membership losses, signalling a potential turnaround in membership growth.

+ 3Q22 beat on both revenue and earnings. 3Q22 revenue of US$7.93bn beat guidance marginally by 1% as a result of outperformance in membership additions offset significantly by FX headwinds. Revenue from UCAN grew 11% YoY, driven mainly by a 12% YoY growth in prices. APAC grew 7% YoY, impacted by a 12% FX headwind. Earnings of US$3.10 also beat guidance by 45% on the back of higher revenue, an estimated US$200mn shift in spend from 3Q22 to 4Q22, and a US$348mn FX remeasurement of the company’s EUR debt. Excluding FX remeasurement, earnings would have beat by around 15%.

+ Strong initial demand from advertisers for new ad-supported plan. Netflix announced that it would be rolling out the much anticipated ad-supported subscription plan to 12 countries this coming Nov at a US$6.99 price point – several months ahead of schedule. Netflix also stated that initial demand from advertisers was very strong, with advertising inventory almost sold out. The company expects this new plan to be margin accretive, and should lead to significant incremental revenue and profit moving forward. The plan is also expected to be neutral to positive on unit economics compared to the existing basic plan.

The Negatives

– Stronger US dollar expected to hurt top and bottom-line growth in 4Q22e. We expect the continued appreciation of the US Dollar relative to most other currencies to continue hurting Netflix’s revenue growth by about 9% in 4Q22e, especially with most of its growth coming from outside the US. We also expect this to affect Operating Margins by about 4%.

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU