NETFLIX INC. - Strong performance overshadowed by weak guidance

26 Jan 2022- 4Q21 results in line with expectations. FY21 revenue/PATMI at 101/105% of our FY21e forecasts.

- Weak 1Q22 guidance on paid net additions due to back-end slated content releases.

- Expected loss of US$1bn in revenue for FY22e due to strengthening US dollar.

- We upgrade to a BUY recommendation with a reduced DCF target price (WACC 9.0%) of US$673.00.

The Positives

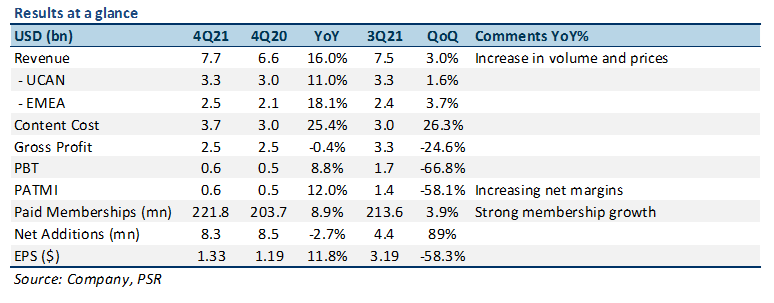

+ Revenue for 4Q21 showed strong growth. NFLX reported revenue of US$7.7bn for 4Q21 – 16% YoY, slightly above our estimates of US$7.5bn. The company also reported FY21 revenue of US$29.7bn – up 19% YoY, slightly above our estimates of US$29.5bn, led by increases in memberships as well as subscription prices.

+ US$1.33 EPS outperformed consensus estimates of US$0.82. NFLX’s EPS of US$1.33 for 4Q21 beat consensus estimates by 62%, largely due to increasing net margins, and a US$104mn non-cash unrealized gain from an FX re-measurement of the company’s euro- denominated debt. EPS for the year was US$11.24, an 85% YoY increase from FY20.

The Negatives

– Weak 1Q22 guidance for paid net additions. NFLX provided relatively weak guidance of 2.5mn net paid additions for 1Q22 vs 4mn in 1Q21. The company attributed this to a continued overhang from COVID-19, a more back-end slated release schedule, as well as macroeconomic strains in the Latin America region.

– Expected revenue loss of US$1bn in FY22e due to strengthening of US dollar. NFLX expects the strengthening of the USD in relation to most other currencies during 2H21 to impact FY22e revenue negatively by US$1bn, representing almost 3% of FY22e revenue. Almost 60% of total revenue is expected to be generated outside of the US, and most of the company’s expenses are within the US, making NFLX susceptible to FX fluctuation risks. In addition, the company does not hedge against this.

Performance

Overall, NFLX’s 4Q21 performance slightly exceeded our 4Q21e forecasts, with outperformances in several areas like net margin (7.9% vs 4.9%) and EPS (US$1.33 vs US$0.81). Paid memberships and paid net additions were slightly below our expectations, but not by much (Figure 1).

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

About the author

Jonathan Woo

Research Analyst

PSR

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.

PayPal Holdings Inc - Consumer spending remains resilient

PayPal Holdings Inc - Consumer spending remains resilient Cromwell European REIT - A resilient 1Q24

Cromwell European REIT - A resilient 1Q24