Raffles Medical - Stock Analyst Research

| Target Price* | 0.96 |

| Recommendation | NEUTRAL› NEUTRAL |

| Market Cap* | - |

| Publication Date | 28 Feb 2024 |

*At the time of publication

Raffles Medical Group Ltd - Lacklustre near-term

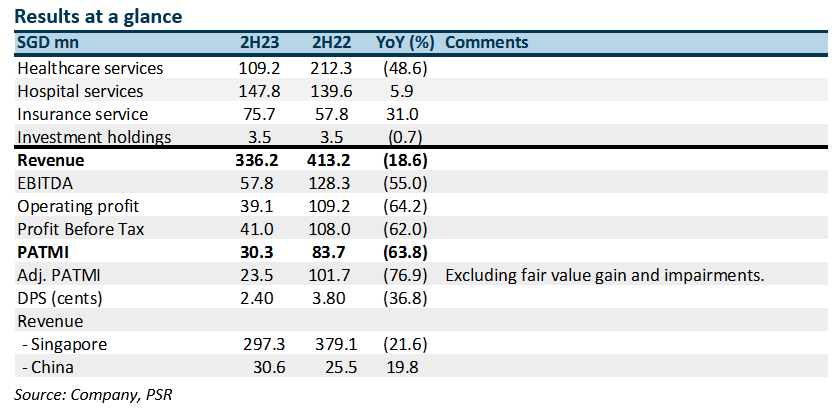

- 2023 earnings were below expectations at 89% of our estimates. 2H23 adjusted PATMI dropped 77% YoY, excluding fair value gains of S$7.4mn.

- The absence of high-margin pandemic-related services such as vaccination and testing was the major drag on earnings. Other activities pulling down margins were lower revenue per bed from transitional care facilities (TCF) and high loss ratios in their insurance business as patient claims normalised.

- We cut our FY24e PATMI by 30% to S$59.2mn. Our NEUTRAL recommendation is maintained, and the DCF target price is lowered to S$0.96 (prev. S$1.02). We do not expect any recovery in margins in the near term. Price pressure from TCF will linger due to aggressive competition. Weakness in foreign patient volume due to the strong Singapore currency, cheaper alternatives, and improved healthcare services in the region. Containing the decline in earnings will be progressive price increases in Singapore hospitals and narrowing losses in China.

The Positive

+ Growth in China. 2023 is effectively the first full year of operation for their new hospital in China, absent the pandemic interruptions. 2H23 revenue grew 20% YoY. Raffles is gradually gaining traction with foreign corporations operating in China. EBITDA break-even will require 2 to 3 years, but patient load is building momentum as marketing efforts intensify.

The Negative

– Revenue and margin collapse. Absent pandemic-related activities, including testing, vaccination, and even TCF, revenue and margins suffered. The pandemic provided extra services for Raffles and margins were high due to the urgency and limited competition.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

Keppel Ltd - A slow quarter

Keppel Ltd - A slow quarter Frasers Centrepoint Trust - Robust operating performance in 1H24

Frasers Centrepoint Trust - Robust operating performance in 1H24 Suntec REIT - Higher-for-longer interest rate continue eroding DPU

Suntec REIT - Higher-for-longer interest rate continue eroding DPU