Venture Corporation Limited-Disrupted quarter

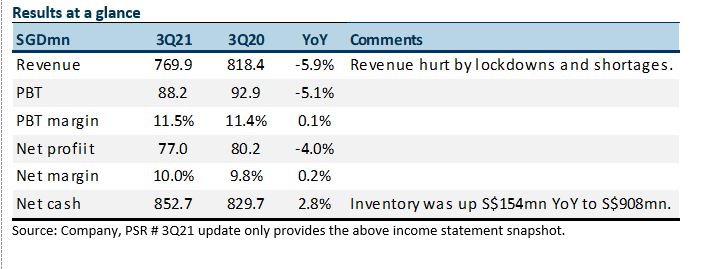

5 Nov 2021- Results were below forecast. 3Q21 PATMI declined 4% YoY to S$77mn. YTD21 Revenue and PATMI were 66% and 63% respectively.

- Fulfilment of customer orders disrupted by global components shortages and the Extended Movement Control Order (or factory closures) in Malaysia.

- We are lowering our FY21e revenue and PATMI by 6% and 10% respectively. Recovery this quarter has been stalled due to production disruptions. The company mentioned that demand is healthy and broad-based demand. In addition, the workforce in Malaysia is almost fully vaccinated, which should allow manufacturing activities to resume as normal. We expect some spill-over of orders into 4Q21. We maintain our NEUTRAL recommendation. Our target price is rolled over to 16x PE FY22e, its 5-year average. Re-opening and removal of lockdown should ease pressure on the supply chain in FY22e. The share price is currently supported by dividend yields of 4.5%, 11% ROEs and S$853mn net cash.

The Positive

+ Healthy balance sheet and margins. Net margins improved marginally to 10%. We assume the high-value low mix projects have been sustaining margins despite the weaker revenue and loss of operating leverage. Net cash was S$853mn at 3Q21. There was a spike in inventory by S$154mn YoY to S$908mn. We believe there is buffer inventory to cope with the unpredictability in component supply.

The Negative

– Another weak quarter in revenue. Pre-pandemic, the quarterly run-rate in revenue was around S$900mn. This has dropped to S$700m this year. Venture has struggled to keep revenues to pre-pandemic levels these past two years despite the global resurgence in electronics demand. The pivot to life science and consequent long timeline to ramp up is a factor, in our opinion. We expect revenue to rebound in 4Q21e to S$916mn, an 11% YoY rise.

Outlook

Venture commented that new product introductions are expected to flow to mass production over the next 12 months.

Maintain NEUTRAL with unchanged TP of S$19.20

Our FY21e and FY22e PATMI is lowered by 10% and 11% respectively

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

About the author

Paul Chew

Head of Research

Phillip Securities Research Pte Ltd

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.

PayPal Holdings Inc - Consumer spending remains resilient

PayPal Holdings Inc - Consumer spending remains resilient Cromwell European REIT - A resilient 1Q24

Cromwell European REIT - A resilient 1Q24