Payroll deduction plan

Table of Contents

Payroll deduction plan

A payroll deduction plan is a valuable financial tool that simplifies employer and employee savings, investment, and benefit contributions. By automating deductions from an employee’s paycheck, this plan encourages disciplined financial habits and facilitates long-term financial security. Employees can benefit from potential tax savings and convenient management of their financial goals and benefits.

What is a payroll deduction plan?

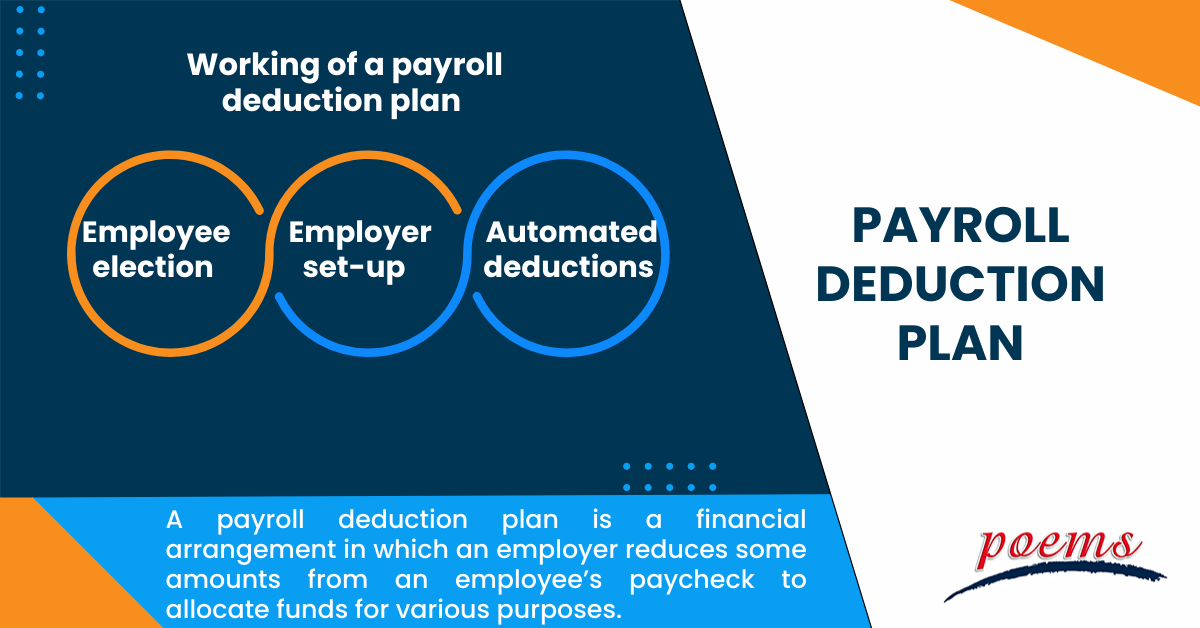

A payroll deduction plan is a financial arrangement in which an employer reduces some amounts from an employee’s paycheck to allocate funds for various purposes. These deductions are typically made before taxes are calculated, allowing employees to take advantage of tax benefits and automate contributions to savings or benefit programs.

Payroll deduction plans are widely used to facilitate employee participation in retirement savings accounts, such as 401(k) plans or IRAs, also called Individual Retirement Accounts. Additionally, employees may use payroll deductions to fund health insurance premiums, flexible spending accounts, or FSAs, charitable donations, and other voluntary benefits the employer offers.

Understanding payroll deduction plans

Payroll deduction plans simplify contributing to various financial accounts and benefits, making saving and investing more convenient for employees. By deducting money directly from an employee’s paycheck, the payroll deduction plan ensures consistent contributions to different accounts, encouraging employees to build financial security.

One of the most common applications of a payroll deduction plan is for retirement savings. Employees can specify a percentage or a fixed amount of their salary to be deducted and contribute to their retirement account. This helps individuals save for their post-retirement years with minimal effort.

Working of a payroll deduction plan

The payroll deduction plan operates by:

- Employee election

The employee decides on the specific deductions they wish to make from their paycheck. This could include retirement contributions, health insurance premiums, charitable donations, or other benefit options.

- Employer set-up

The employer processes the employee’s request and sets up the appropriate deductions in the payroll system. This ensures that the specified amounts are withheld from the employee’s gross pay before taxes are calculated.

- Automated deductions

Each pay period automatically deducts the specified amounts from the employee’s gross pay, and the net amount is deposited into the employee’s bank account.

Benefits of payroll deduction plan

Payroll deduction plans offer several benefits to both employers and employees:

- Simplified savings

Employees can effortlessly contribute to savings and investment accounts without remembering to make separate transfers.

- Pre-tax contributions

Deductions made before calculating taxes reduce the employee’s taxable income, resulting in potential tax savings.

- Financial discipline

The automatic nature of payroll deductions encourages disciplined saving and investment behaviour.

- Convenience

Employees can manage their finances effectively with automated contributions to various accounts and benefits.

- Employee retention

Offering payroll deduction plans can enhance employee satisfaction and retention, especially for retirement savings.

- Administrative efficiency

Automated payroll deductions streamline administrative processes, reducing the workload for HR and payroll departments.

- Employee incentive

Payroll deduction plans can be used as an incentive to attract and retain talent by providing valuable benefits to employees.

- Financial safety

Employees can improve their financial stability and be better prepared for future demands by contributing to retirement funds or emergency funds through payroll deductions.

- Repayment of debt

Payroll deductions can be utilised to allocate funds into debt repayment, allowing employees to manage and minimise their obligations better.

- Legal compliance

Some deductions, such as healthcare premium or retirement payments, may be legally required. Using a payroll deduction system aids in ensuring compliance with applicable rules.

- Employee satisfaction and retention

Implementing payroll deduction plans, particularly for retirement savings, may raise employee satisfaction and organisational commitment, lowering turnover.

Example of payroll deduction plan

Let’s consider an example of how a payroll deduction plan works for an employee named John:

John earns a gross monthly salary of US$4,000 and wants to contribute 5% to a 401(k) retirement plan. He also decides to allocate US$100 monthly to a health savings account, or HSA, to cover medical expenses tax-free.

With a payroll deduction plan in place:

John’s monthly salary: US$4,000

Retirement plan contribution (5% of US$4,000): US$200 (pre-tax deduction)

HSA contribution: US$100 (pre-tax deduction)

Calculation:

Gross salary: US$4,000

Retirement plan contribution: -US$200

HSA contribution: US$100

Taxable income: US$3,700 (US$4,000 – US$200 – US$100)

John’s taxes will be calculated based on the taxable income of US$3,700 instead of US$4,000, reducing his tax liability. The US$200 contribution to his retirement plan and the US$100 contribution to his HSA will be automatically deposited into their respective accounts.

Frequently Asked Questions

The payroll deduction process involves deducting specific amounts from an employee’s paycheck before calculating taxes. These deductions can include contributions to retirement plans, health insurance premiums, flexible spending accounts, charitable donations, and other benefits chosen by the employee.

An individual retirement account funded through automatic deductions from an employee’s paycheck is termed as a payroll deduction IRA. It allows employees to contribute to their retirement savings regularly, making building a nest egg for retirement easier.

A deduction from salary for an employee refers to the amount withheld from the employee’s gross pay to cover various expenses or contributions, such as taxes, retirement savings, health insurance premiums, and other benefit programs.

In payroll accounting, various items of deductions include:

- Federal, state, and local taxes

- Social Security and Medicare contributions

- Retirement plan contributions

- Health insurance premiums

- Flexible spending account contributions

- Charitable donations

- Union dues (if applicable)

- Other benefit program contributions

While it is impossible to avoid paying taxes on salary completely, employees can take advantage of pre-tax deductions through programs like 401(k) plans, HSAs, and flexible spending accounts. These deductions reduce the taxable income, leading to potential tax savings. Additionally, tax credits and deductions available through the tax code can lower overall tax liability. However, it is essential to comply with tax and seek advice from a tax professional to ensure proper tax planning and compliance.

Related Terms

- Cost of Equity

- Capital Adequacy Ratio (CAR)

- Interest Coverage Ratio

- Industry Groups

- Income Statement

- Historical Volatility (HV)

- Embedded Options

- Dynamic Asset Allocation

- Depositary Receipts

- Deferment Payment Option

- Debt-to-Equity Ratio

- Financial Futures

- Contingent Capital

- Conduit Issuers

- Calendar Spread

- Cost of Equity

- Capital Adequacy Ratio (CAR)

- Interest Coverage Ratio

- Industry Groups

- Income Statement

- Historical Volatility (HV)

- Embedded Options

- Dynamic Asset Allocation

- Depositary Receipts

- Deferment Payment Option

- Debt-to-Equity Ratio

- Financial Futures

- Contingent Capital

- Conduit Issuers

- Calendar Spread

- Devaluation

- Grading Certificates

- Distributable Net Income

- Cover Order

- Tracking Index

- Auction Rate Securities

- Arbitrage-Free Pricing

- Net Profits Interest

- Borrowing Limit

- Algorithmic Trading

- Corporate Action

- Spillover Effect

- Economic Forecasting

- Treynor Ratio

- Hammer Candlestick

- DuPont Analysis

- Net Profit Margin

- Law of One Price

- Annual Value

- Rollover option

- Financial Analysis

- Currency Hedging

- Lump sum payment

- Annual Percentage Yield (APY)

- Excess Equity

- Fiduciary Duty

- Bought-deal underwriting

- Anonymous Trading

- Fair Market Value

- Fixed Income Securities

- Redemption fee

- Acid Test Ratio

- Bid Ask price

- Finance Charge

- Futures

- Basis grades

- Short Covering

- Visible Supply

- Transferable notice

- Intangibles expenses

- Strong order book

- Fiat money

- Trailing Stops

- Exchange Control

- Relevant Cost

- Dow Theory

- Hyperdeflation

- Hope Credit

- Futures contracts

- Human capital

- Subrogation

- Qualifying Annuity

- Strategic Alliance

- Probate Court

- Procurement

- Holding company

- Harmonic mean

- Income protection insurance

- Recession

- Savings Ratios

- Pump and dump

- Total Debt Servicing Ratio

- Debt to Asset Ratio

- Liquid Assets to Net Worth Ratio

- Liquidity Ratio

- Personal financial ratios

- Operating expenses

- Demand elasticity

- Deferred compensation

- Conflict theory

- Acid-test ratio

- Withholding Tax

- Benchmark index

- Double Taxation Relief

- Debtor Risk

- Securitization

- Yield on Distribution

- Currency Swap

- Overcollateralization

- Efficient Frontier

- Listing Rules

- Green Shoe Options

- Accrued Interest

- Market Order

- Accrued Expenses

- Target Leverage Ratio

- Acceptance Credit

- Balloon Interest

- Abridged Prospectus

- Data Tagging

- Perpetuity

- Optimal portfolio

- Hybrid annuity

- Investor fallout

- Intermediated market

- Information-less trades

- Back Months

- Adjusted Futures Price

- Expected maturity date

- Excess spread

- Quantitative tightening

- Accreted Value

- Equity Clawback

- Soft Dollar Broker

- Stagnation

- Replenishment

- Decoupling

- Holding period

- Regression analysis

- Wealth manager

- Financial plan

- Adequacy of coverage

- Actual market

- Credit risk

- Insurance

- Financial independence

- Annual report

- Financial management

- Ageing schedule

- Global indices

- Folio number

- Accrual basis

- Liquidity risk

- Quick Ratio

- Unearned Income

- Sustainability

- Value at Risk

- Vertical Financial Analysis

- Residual maturity

- Operating Margin

- Trust deed

- Profit and Loss Statement

- Junior Market

- Affinity fraud

- Base currency

- Working capital

- Individual Savings Account

- Redemption yield

- Net profit margin

- Fringe benefits

- Fiscal policy

- Escrow

- Externality

- Multi-level marketing

- Joint tenancy

- Liquidity coverage ratio

- Hurdle rate

- Kiddie tax

- Giffen Goods

- Keynesian economics

- EBITA

- Risk Tolerance

- Disbursement

- Bayes’ Theorem

- Amalgamation

- Adverse selection

- Contribution Margin

- Accounting Equation

- Value chain

- Gross Income

- Net present value

- Liability

- Leverage ratio

- Inventory turnover

- Gross margin

- Collateral

- Being Bearish

- Being Bullish

- Commodity

- Exchange rate

- Basis point

- Inception date

- Riskometer

- Trigger Option

- Zeta model

- Racketeering

- Market Indexes

- Short Selling

- Quartile rank

- Defeasance

- Cut-off-time

- Business-to-Consumer

- Bankruptcy

- Acquisition

- Turnover Ratio

- Indexation

- Fiduciary responsibility

- Benchmark

- Pegging

- Illiquidity

- Backwardation

- Backup Withholding

- Buyout

- Beneficial owner

- Contingent deferred sales charge

- Exchange privilege

- Asset allocation

- Maturity distribution

- Letter of Intent

- Emerging Markets

- Consensus Estimate

- Cash Settlement

- Cash Flow

- Capital Lease Obligations

- Book-to-Bill-Ratio

- Capital Gains or Losses

- Balance Sheet

- Capital Lease

Most Popular Terms

Other Terms

- Bond Convexity

- Compound Yield

- Brokerage Account

- Discretionary Accounts

- Industry Groups

- Growth Rate

- Green Bond Principles

- Gamma Scalping

- Funding Ratio

- Free-Float Methodology

- Foreign Direct Investment (FDI)

- Floating Dividend Rate

- Flight to Quality

- Real Return

- Protective Put

- Perpetual Bond

- Option Adjusted Spread (OAS)

- Non-Diversifiable Risk

- Merger Arbitrage

- Liability-Driven Investment (LDI)

- Income Bonds

- Guaranteed Investment Contract (GIC)

- Flash Crash

- Equity Carve-Outs

- Cost Basis

- Deferred Annuity

- Cash-on-Cash Return

- Earning Surprise

- Bubble

- Beta Risk

- Bear Spread

- Asset Play

- Accrued Market Discount

- Ladder Strategy

- Junk Status

- Intrinsic Value of Stock

- Interest-Only Bonds (IO)

- Inflation Hedge

- Incremental Yield

- Industrial Bonds

- Holding Period Return

- Hedge Effectiveness

- Flat Yield Curve

- Fallen Angel

- Exotic Options

- Execution Risk

- Exchange-Traded Notes

- Event-Driven Strategy

- Eurodollar Bonds

- Enhanced Index Fund

Know More about

Tools/Educational Resources

Markets Offered by POEMS

Read the Latest Market Journal

How CFDs Complement Your Trading and Investing Strategies

How CFDs Complement Your Trading and Investing Strategies In today’s fast-moving financial markets, investors and traders are constantly seeking ways to improve their strategies and capture to new opportunities. Contracts for Difference (CFDs) have become a popular tool because they offer flexibility, access to global markets, and the ability to trade both rising and falling prices. However, CFDs are complex, leveraged products that carry a higher level of risk and may not be suitable for all investors. What Are CFDs? A Contract for Difference (CFD) is a derivative product that allows you to participate in the price movement of an asset without owning the underlying assets.1 Instead of purchasing the asset, you initiate an agreement with a CFD broker to settle the difference between the opening and closing prices of your position. CFDs also allow you to trade a variety of asset classes within a single account, making them a flexible and versatile tool for enhancing both trading and investing strategies. How CFDs Complement Trading Strategies? For traders, CFDs provide opportunities that may not always be available in traditional markets. Their flexibility and fast execution make them well suited for short-term strategies such as day trading, swing trading, and scalping. Leverage for Capital Efficiency CFDs allow traders to improve their capital efficiency as they are traded on margin. This means traders can initiate positions with a smaller initial capital outlay. As a result, this increases accessibility to financial markets, especially for those with limited capital. However, leverage also amplifies losses, making proper risk management essential,2 which we will explore in more detail later. Example: If a trader wants to gain exposure to shares worth US$10,000, using 10:1 leverage they would only need to provide US$1,000 as margin. By applying proper risk management, such as limiting the trade to a small portion of total capital and using stop-loss orders, potential losses can be controlled while still benefiting from leverage. Positioning for Rising or Falling Markets One notable advantage of CFDs is the ability to short sell. This enables traders to manage their positions and potentially generate profits or mitigate losses during periods of market decline. Downward movements can be especially pronounced during risk-off phases, and CFDs offer flexibility for traders to adopt either long or short positions. When market sentiment turns negative, sharp declines in price may occur, presenting opportunities for traders seeking to capitalize on strong, short-term momentum. With the ability to short sell through CFDs, traders can take advantage of these downward moves rather than missing potential opportunities when markets drop.3 Access to Multiple Global Market When trading CFDs, traders can access multiple global markets through a single trading account rather than opening separate accounts for each market4. As global markets operate across different time zones, this access allows traders to participate in markets at various times throughout the day. This creates a more continuous flow of opportunities, particularly during periods of heightened volatility. How CFDs Complement Investing Strategies? CFDs are often associated with short-term trading. However, when structured effectively, they can enhance long-term investing strategies. They are not meant to replace traditional investing, instead, they act as a strategic tool to improve flexibility, capital efficiency, and risk management. 1) Adding Tactical Opportunities to a Portfolio Long-term investors build portfolios based on strategic asset allocation, selecting quality investments to hold for several years and benefit from sustained market growth. However, markets do not move in a straight line, and short-term volatility can arise from economic data releases, sector forward narrative, and global events. CFDs offer a way for investors to take advantage of these shorter-term market movements without altering their core long-term holdings. 2) Hedging Long-Term Positions Hedging is a risk management strategy that involves taking positions designed to offset potential losses in an existing investment portfolio5. Market volatility is an unavoidable part of investing. Unexpected events such as economic uncertainty, geopolitical developments, and changes in interest rates may include a financial shock, triggering market corrections. These occurrences can disrupt market stability and lead to significant fluctuations in asset prices. Instead of selling long-term holdings during periods of uncertainty, investors can use CFDs to hedge their exposure. For example, if an investor holds a portfolio of technology stocks and expects short-term market weakness, they may open a short CFD position on technology stock or index. If the market declines, the losses in the portfolio may be partially offset by gains from the CFD position. This allows investors to manage short-term downside risk while continuing to hold their long-term investments6. 3) Capital Efficiency and Diversification Unlike traditional investing, CFDs require only margin rather than the full capital outlay of the underlying asset. This allows investors to gain market exposure while keeping more capital available for other opportunities. In addition, CFDs provide new investment opportunities beyond traditional exchange-traded products such as foreign exchange (FX), global indices, and commodities. This allows long-term investors to broaden their exposure to different asset classes without trading directly in those markets7. As financial markets move rapidly, opportunities may arise unexpectedly. If capital is fully committed to long-term positions, investors may miss these opportunities. By incorporating CFDs, investors can maintain greater flexibility while continuing to participate in the markets. Key Considerations: Risks of Trading CFDs CFDs are leveraged financial instruments and carry a higher level of risk compared to traditional investments. Even small price movements in the underlying asset can have a significant impact on a trader’s position. As a result, both gains and losses are magnified. Therefore, it is important for investors and traders to understand the potential risks and apply proper risk management when trading CFDs8. Leverage Risk – Leverage allows traders to control larger positions with less capital, but it can also amplify losses and the losses may exceed initial capital if the market moves against the trade. Market Volatility – Sudden market movements caused by economic news or geopolitical events can lead to rapid price changes and unexpected losses. Margin Call Risk – If account equity falls below the required margin level, traders may need to add funds or risk having positions forced closed. Overnight Financing Costs – Holding CFD positions overnight may incur financing charges, which can affect overall profitability. Mitigating Risks and Best Practices To manage these risks effectively, traders should adopt disciplined practices: traders should set stop-loss and take-profit levels to define clear exit points9 and conservative position sizes, diversify across various markets and asset classes, and monitor positions regularly. New traders are advised to start with smaller trades or demo accounts to gain experience, as well as periodically review and adjust strategies to respond to changing market conditions. Conclusion CFDs are versatile financial instruments that can add value to both trading and investing strategies. For traders, they offer provide ease of trade, leverage, and the ability to profit in rising or falling markets. For investors, CFDs can enhance portfolio flexibility, support hedging strategies, and flexibility in managing portfolios. Whether you are seeking to capture short-term opportunities or manage long-term portfolio risks, CFDs can serve as a valuable tool within a broader financial strategy. When used responsibly, they can help bridge the gap between active trading and long-term wealth accumulation. Promotion Start your CFD journey with us and enjoy 0 commission on US equity CFDs for 30 days when you open a CFD account with us. In addition, receive S$50 cash credit when you fund and trade. As long as you open a POEMS CFD Account during the promotion period of 10 March 2026 to 10 June 2026 (both dates inclusive) and do NOT have any existing POEMS CFD Account(s), your 0 commission on US Equity CFDs for 30 days will be active upon receiving an email notification to indicate promotion has been activated for the account. For more information, you can visit our CFD website or click here References: Understanding contracts for difference. (n.d.). https://www.moneysense.gov.sg/understanding-contracts-for-difference/ MarketMates. (2024, August 13). Trading 101: Leverage and margin explained. https://marketmates.com/learn/cfd-trading/trading-101-leverage-and-margin-explained/ Phillip CFD. (2021a, March 16). What is Short-Selling? | CFD Trading Singapore | Phillip CFD. https://www.phillipcfd.com/products/what-is-short-selling/ What is CFD trading – a beginner’s guide. (2026, January 12). TradingView. https://www.tradingview.com/news/forexlive:704a82432094b:0-what-is-cfd-trading-a-beginner-sguide/#:~:text=Types%20of%20CFD%20Markets,%2C%20and%20Ripple%20(XRP) Popular hedging Strategies for traders in 2025 for FXOPEN:EURUSD by FXOpen. (2025, March 19). TradingView. https://www.tradingview.com/chart/EURUSD/oeOYrKIr-Popular-Hedging-Strategies-for-Traders-in-2025/ Hedging in Share Market | Types of Hedging Strategies in Trading. (n.d.). https://www.truedata.in/blog/hedging-in-share-market? Gratton, P. (2025, August 28). Understanding Contract for Differences (CFDs): Key insights and benefits. Investopedia. https://www.investopedia.com/articles/stocks/09/trade-a-cfd.asp What is CFD trading – a beginner’s guide. (2026b, January 12). TradingView. https://www.tradingview.com/news/forexlive:704a82432094b:0-what-is-cfd-trading-a-beginner-s-guide/ Gratton, P. (2025b, August 28). Understanding Contract for Differences (CFDs): Key insights and benefits. Investopedia https://www.investopedia.com/articles/stocks/09/trade-a-cfd.asp Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Q&M Dental Group Poised for Major Expansion Through Strategic Acquisitions

Company Overview Q&M Dental Group Ltd operates as a dental services provider with a current network of more than 150 standalone clinics in Singapore and Malaysia. The company is positioning itself to become a major dental franchise platform through strategic acquisitions and organic growth initiatives. Ambitious Acquisition Strategy The company has announced three significant proposed acquisitions totalling approximately S$272 million, which could potentially double its earnings upon completion. These acquisitions span across Australia, Singapore, and Thailand, backed by robust profit guarantees totalling S$200 million over five to eight years. The largest acquisition involves an Australian dental network valued at A$144.5 million (approximately S$130 million), comprising more than 40 clinics and 120 dentists. This will be complemented by additional Singapore clinic acquisitions and a Thai operation focused on cosmetic and aesthetic dentistry with over 30 clinics. Financing Structure and Growth Projections The acquisitions will be financed through a combination of cash and shares, following the Australian acquisition template where 40% of the purchase consideration will be satisfied through shares issued at S$0.70. Notably, the structure includes a 15-year moratorium on shares and service agreements to ensure vendor alignment with long-term objectives. The profit guarantees provide embedded earnings growth of approximately 14% per annum over the next three years. These acquisitions are expected to boost FY26 estimated earnings per share by 80% to 3.5 cents. Operational Synergies and Network Expansion The expanded network will create opportunities for revenue and cost synergies, alongside the implementation of best practices in marketing, advanced dentistry, and operations. The company aims to aggressively grow the Australian network towards 400 clinics over five years, whilst targeting 300 dental clinics across Singapore over the same period. The broader network will also serve as a platform for rolling out EM2AI solutions. Financial Performance and Outlook FY25 revenue exceeded expectations at 105% with the consolidation of Aoxin Q&M, though net profit came in at 68% due to S$2.4 million in interest expenses and S$2 million in one-off costs. Additional government subsidies for restorative dental procedures introduced in October contributed a 3% boost to Singapore revenue in the second half of FY25. Phillip Securities Research Recommendation Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.71 (previously S$0.545). The fair value post-acquisition is estimated at S$0.95, though a 50% discount has been applied pending completion of the acquisitions. The valuation is pegged at 25x PE FY26, in line with the Singapore healthcare sector. Frequently Asked Questions Q: What is the total value of Q&M Dental's proposed acquisitions? A: The three proposed acquisitions have an estimated total value of S$272 million, covering dental operations in Australia, Singapore, and Thailand. Q: How will these acquisitions be financed? A: The acquisitions will be satisfied through a combination of cash and shares, with 40% of the purchase consideration in shares issued at S$0.70, following the Australian acquisition template. Q: What are the profit guarantees associated with these acquisitions? A: The acquisitions are backed by profit guarantees totalling S$200 million over five to eight years, providing embedded earnings growth of approximately 14% per annum for the next three years. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.71, up from the previous target of S$0.545. Q: How many clinics does Q&M currently operate and what are its expansion plans? A: Q&M currently operates more than 150 clinics in Singapore and Malaysia and aims to grow towards 300 dental clinics in Singapore and 400 clinics in Australia over the next five years. Q: What impact will the acquisitions have on earnings? A: The acquisitions are estimated to boost FY26 earnings per share by 80% to 3.5 cents, with the potential to double the company's overall earnings upon completion. Q: What operational benefits are expected from the acquisitions? A: The expanded network will create opportunities for revenue and cost synergies, implementation of best practices in marketing and operations, and serve as a platform for rolling out EM2AI solutions across the broader clinic network. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Micron Technology Reports Record Quarterly Performance Amid Strategic Shifts

Company Overview Micron Technology, Inc is a leading global semiconductor company specialising in memory and storage solutions, including DRAM and NAND flash memory products that are essential components in various electronic devices and data centres. Strong Financial Performance Drives Optimism Micron Technology has delivered exceptional financial results for the second quarter of fiscal year 2026, with adjusted profit after tax and minority interests (PATMI) surging 686% year-on-year to a record US$14 billion. This remarkable performance was driven by substantial bit shipment growth of approximately 35% year-on-year, combined with significant increases in average selling prices (ASPs) for both DRAM and NAND memory products, which rose an estimated 107% and 118% respectively. The company's revenue performance aligned with analyst expectations, with first-half fiscal 2026 revenue representing 50% of the full-year forecast. Meanwhile, the adjusted PATMI exceeded expectations, accounting for 58% of the annual projection, indicating strong momentum in the business. Strategic Customer Agreements Signal Market Evolution A significant development for Micron has been the establishment of its first five-year strategic customer agreement (SCA) with an undisclosed large customer. This represents a notable shift from the company's traditional approach of securing long-term agreements that typically last only one year. The move reflects the evolving landscape in the semiconductor industry, where high-end chipmakers and hyperscalers increasingly view memory as strategically critical in the artificial intelligence race, leading to longer-term contractual commitments across the sector. Market Outlook and Geopolitical Considerations Phillip Securities Research maintains a BUY recommendation with an upgraded target price of US$530, increased from the previous US$500. The research house has raised its fiscal 2026 revenue and PATMI forecasts by 43% and 100% respectively, citing an ongoing industry shortage in memory chips that is expected to continue pushing DRAM and NAND ASPs higher. However, the analysis incorporates geopolitical risk factors, particularly concerns about potential disruptions from Middle East conflicts. The research notes that closure of the Straits of Hormuz could threaten 30% of global helium supply, a critical component in semiconductor wafer manufacturing. Micron is considered better positioned than Korean competitors due to its stronger presence in the United States, which accounts for approximately 45% of global helium production compared to Qatar's 30%. Frequently Asked Questions Q: What drove Micron's record quarterly performance? A: The record US$14 billion adjusted PATMI was driven by bit shipment growth of approximately 35% year-on-year and significant increases in DRAM and NAND average selling prices, which rose an estimated 107% and 118% respectively. Q: How significant is Micron's new strategic customer agreement? A: This is Micron's first five-year strategic customer agreement, representing a major shift from traditional long-term agreements that typically last only one year, reflecting the strategic importance of memory in the AI race. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY recommendation with a target price of US$530, upgraded from the previous US$500. Q: How much did analysts raise their forecasts? A: Phillip Securities Research’s analysts raised fiscal 2026 revenue forecasts by 43% and PATMI forecasts by 100%. Q: What supply outlook does the research anticipate? A: Industry supply is expected to increase meaningfully starting from the second half of calendar year 2027, as SK Hynix aims to maintain its 2026 capital expenditure-to-sales ratio at approximately mid-30% level. Q: What geopolitical risks affect Micron? A: Potential closure of the Straits of Hormuz could threaten 30% of global helium supply, critical for semiconductor manufacturing, though Micron is considered better positioned than Korean competitors due to stronger US presence. Q: How does Micron's geographic positioning help with supply chain risks? A: Micron benefits from stronger presence in the United States, which accounts for about 45% of global helium production compared to Qatar's 30%, providing better insulation from Middle East conflicts than Korean competitors. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Singapore REITs Show Resilience Despite February Decline

Market Performance and Sector Overview Singapore Real Estate Investment Trusts (S-REITs) experienced a modest setback in February 2026, with the S-REITs Index declining 1.9% after posting a 0.7% gain in January. This correction reflects broader market volatility amid ongoing geopolitical tensions and monetary policy uncertainty. The S-REITs sector encompasses a diverse portfolio of real estate investments, including retail properties in Singapore and commercial assets overseas. These investment vehicles provide investors with exposure to income-generating real estate across multiple geographic markets and property types, offering regular dividend distributions and portfolio diversification benefits. Individual REIT Performance Performance varied significantly across individual REITs during February. Stoneweg Europe Stapled Trust emerged as the standout performer, surging 6.9% following strong full-year 2025 results. Conversely, Prime US REIT faced headwinds, declining 12.9% after the previous month's 14.2% rally, as investors reassessed the pace of occupancy recovery within its portfolio. Sub-sector performance also diverged notably. Singapore retail REITs led gains with a 0.8% increase, demonstrating the resilience of domestic retail properties. However, overseas commercial properties struggled, particularly US office S-REITs, which contributed to an 8% decline in the overseas commercial sub-sector. Interest Rate Environment and Growth Prospects Despite inflationary pressures stemming from Middle East geopolitical tensions and Federal Reserve expectations of maintaining elevated interest rates, analysts identify potential catalysts for stronger distribution per unit growth in financial year 2026. The continued decline in benchmark Singapore Overnight Rate Average rates is expected to generate meaningful interest cost savings for S-REITs, supporting improved financial performance. Investment Outlook and Recommendations Phillip Securities Research maintains an OVERWEIGHT recommendation on S-REITs, citing their stable performance and defensive characteristics as attractive features for global investors navigating market uncertainty. The sector's valuation metrics remain compelling, trading at a forward dividend yield spread of approximately 3.8% and a price-to-net asset value ratio of 0.97 times. Within sub-sectors, retail properties are favoured due to expectations of strong rental reversions in the high single digits throughout 2026. Overseas S-REITs offering yields exceeding 8% with resilient portfolios are also preferred, including specific recommendations for Stoneweg Europe Stapled Trust with a target price of €1.89, Elite UK REIT at £0.41, United Hampshire US REIT at US$0.69, and Prime US REIT at US$0.32. Frequently Asked Questions Q: What was the performance of Singapore REITs in February 2026? A: The S-REITs Index fell 1.9% in February 2026, reversing the 0.7% gain recorded in January 2026. Q: Which REIT was the best performer in February and why? A: Stoneweg Europe Stapled Trust was the top performer, rising 6.9% on strong FY25 results. Q: What is Phillip Securities Research's overall recommendation on S-REITs? A: Phillip Securities Research maintains an OVERWEIGHT recommendation on S-REITs due to their stable performance and defensive positioning. Q: Which sub-sectors are preferred and why? A: Retail is preferred due to expected strong rental reversions in the high single digits in 2026, and overseas S-REITs offering high yields over 8% with resilient portfolios are also favoured. Q: What are the key target prices mentioned in the report? A: Target prices include Stoneweg Europe Stapled Trust at €1.89, Elite UK REIT at £0.41, United Hampshire US REIT at US$0.69, and Prime US REIT at US$0.32. Q: What factors support potential DPU growth in FY26? A: Interest cost savings from declining benchmark SORA rates are expected to support stronger distribution per unit growth in FY26. Q: How are S-REITs currently valued? A: The sector trades at a forward dividend yield spread of approximately 3.8% and a price-to-net asset value ratio of 0.97 times, which are considered undemanding valuations. Q: What challenges does the sector face? A: The sector faces inflation concerns from heightened geopolitical tensions in the Middle East and expectations that the Federal Reserve will maintain higher-for-longer interest rates. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Wee Hur Holdings Upgraded to Buy on Strong Performance and Growth Prospects

Company Overview Wee Hur Holdings Ltd is a Singapore-based company operating across three key business segments: worker dormitory operations, building construction, and property development. The company has established itself as a significant player in Singapore's infrastructure and accommodation sectors, with substantial dormitory assets and a growing construction order book. Strong Financial Performance Drives Upgrade Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, raising the target price to S$1.08 from S$0.90 previously. This upgrade follows exceptional 2H25 results that significantly exceeded expectations, with revenue and adjusted PATMI reaching 114% and 138% of full-year forecasts respectively. The company's adjusted PATMI surged 81% year-on-year to S$50 million in 2H25, driven by multiple growth catalysts across its business segments. The strong performance reflects successful execution of the company's diversified business model and strategic positioning in Singapore's infrastructure development. Worker Dormitory Business Anchors Growth The worker dormitory segment delivered robust performance, with Tuas View Dormitory achieving 95% occupancy compared to 93% in FY24, alongside positive rental revisions of approximately 5% year-on-year. The segment benefited significantly from Pioneer Lodge's Phase 1 operations, which added 3,088 beds representing a 20% capacity increase since May 2025. This expansion drove dormitory revenue up 21% year-on-year to S$50.8 million in 2H25. Pioneer Lodge's Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to contribute to occupancy ramp-up in FY26. Construction Segment Shows Marked Improvement The building construction segment demonstrated remarkable turnaround, with revenue spiking 172% year-on-year to S$50 million in 2H25. Operating margins improved substantially by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24. This improvement was driven by higher recognition of external projects, which now comprise 99% of the company's S$673 million order book, up from 59% previously. The expanded order book, growing from S$263 million in FY24, is expected to support construction segment growth through 4Q29. Strategic Portfolio Adjustments The research firm's sum-of-the-parts valuation model reflects strategic portfolio changes, including the removal of Mega@Woodlands property development and the addition of Wee Hur's 50% stake in the S$614 million Upper Thomson Road GLS site. The model also incorporates the company's estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III, backed by a 708-bed Australia PBSA. Future Outlook With major construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort on the horizon, analysts expect Wee Hur's 15,744-bed Tuas View Dormitory lease to be extended beyond November 2026, providing continued revenue visibility for the dormitory business. Frequently Asked Questions Q: What is Phillip Securities Research's current recommendation and target price for Wee Hur Holdings? A: Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, with a higher target price of S$1.08, increased from the previous target of S$0.90. Q: How did Wee Hur's 2H25 results compare to expectations? A: The company's 2H25 revenue and adjusted PATMI significantly exceeded expectations, reaching 114% and 138% of full-year forecasts respectively, with adjusted PATMI surging 81% year-on-year to S$50 million. Q: What drove the strong performance in the worker dormitory segment? A: The dormitory segment benefited from Tuas View Dormitory's improved occupancy rate of 95% and positive rental revisions of about 5% year-on-year, plus contributions from Pioneer Lodge Phase 1's additional 3,088 beds, driving dormitory revenue up 21% year-on-year to S$50.8 million. Q: How has the building construction segment's profitability changed? A: The building construction segment's operating margins improved significantly by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24, driven by higher recognition of external projects and an expanded order book. Q: What is the current size and composition of Wee Hur's construction order book? A: The company's construction order book stands at S$673 million, up from S$263 million in FY24, with external projects now comprising 99% of the order book compared to 59% previously. This order book is expected to support growth through 4Q29. Q: When will Pioneer Lodge Phase 2 contribute to operations? A: Pioneer Lodge Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to ramp up occupancy in FY26. Q: What major construction projects could benefit Wee Hur's dormitory business? A: Major upcoming construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort are expected to support the extension of Wee Hur's 15,744-bed Tuas View Dormitory lease beyond November 2026. Q: What changes were made to the valuation model? A: The sum-of-the-parts model removed Mega@Woodlands property development and included Wee Hur's 50% stake in the S$614 million Upper Thomson Road GLS site, plus the company's estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III backed by a 708-bed Australia PBSA. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

TeleChoice International Ltd Maintains Growth Trajectory with Strong FY25 Performance

Company Overview TeleChoice International Ltd is a telecommunications services provider focused on personal communications systems (PCS) and network engineering services. The company operates across Southeast Asia, with significant exposure to Malaysia's telecommunications market through its partnership with U-Mobile. Financial Performance Exceeds Expectations TeleChoice delivered FY25 results that met analyst forecasts, with revenue and profit after tax and minority interests (PATMI) reaching 105% and 103% of expectations respectively. Revenue expanded substantially by 27% year-on-year to S$276 million, primarily supported by U-Mobile 4PL services. However, adjusted PATMI grew at a more modest 20% year-on-year to S$4.4 million due to inventory provisioning impacts. Shareholders benefited from a significant dividend increase, with FY25 dividends more than tripling to 0.45 cents. Personal Communications System Drives Growth The personal communications system segment remained the company's primary growth engine, with revenue surging 42% year-on-year to S$200 million. This impressive growth was fuelled by U-Mobile's expanding subscriber base and the increasing adoption of higher-value postpaid plans requiring handset subsidies. TeleChoice strategically expanded its retail footprint by increasing outlet numbers, broadening its device portfolio, and introducing additional accessories to capture greater market share. Challenges and Outlook Despite the strong revenue performance, TeleChoice faced headwinds from higher inventory provisions. The company experienced a significant spike in inventory write-downs, with provisions increasing by S$2.5 million to S$3.8 million. This provisioning was attributed to a S$11 million year-on-year rise in inventory levels during FY25, compared to S$9.3 million in FY24. Research Recommendation and Valuation Phillip Securities Research maintains its BUY recommendation on TeleChoice International, raising the target price to S$0.275 from the previous S$0.215. The firm increased its FY26e PATMI forecast by 13% to S$8.3 million. The valuation is based on a 15x price-to-earnings multiple for FY26e, benchmarked against SGX-listed companies in the system integration and software sectors. The research house noted that growth momentum in PCS remains intact, with network engineering showing signs of recovery through managed services and network buildout projects in Indonesia and Malaysia. Additionally, TeleChoice is evaluating expansion opportunities into higher-growth digital infrastructure segments, including data centres. Frequently Asked Questions Q: What were TeleChoice's key financial results for FY25? A: TeleChoice achieved revenue of S$276 million, representing 27% year-on-year growth, and adjusted PATMI of S$4.4 million, up 20% year-on-year. Results were within expectations at 105% and 103% of forecasts respectively. Q: Which business segment drove the strongest growth? A: The personal communications system (PCS) segment was the key growth driver, with revenue jumping 42% year-on-year to S$200 million, supported by U-Mobile subscriber growth and higher postpaid plans. Q: What challenges did the company face during FY25? A: TeleChoice experienced higher inventory provisions, with write-downs increasing by S$2.5 million to S$3.8 million due to a S$11 million year-on-year rise in inventory levels. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.275, up from the previous S$0.215, based on 15x P/E for FY26e. Q: How did dividends perform in FY25? A: FY25 dividends more than tripled to 0.45 cents, representing a 260% increase from the previous year's 0.125 cents. Q: What expansion opportunities is TeleChoice considering? A: The company announced it is evaluating expansion into higher-growth segments within digital infrastructure, including data centres, whilst network engineering is recovering through managed services and projects in Indonesia and Malaysia. Q: What factors contributed to the PCS segment's strong performance? A: Growth was driven by U-Mobile 5G subscribers, additional retail stores, postpaid handset subsidies, a widening range of devices, and expanded accessories offerings. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Singapore Banking Sector Faces Mixed Outlook as Rates Stabilise

Interest Rate Environment Shows Signs of Stabilisation Singapore's banking sector is navigating a transitional period as interest rate declines begin to moderate. Feb's 3-month Singapore Overnight Rate Average (3M-SORA) fell by just 2 basis points month-on-month to 1.16%, marking the smallest monthly decline in 20 months. Year-on-year, the rate decreased by 168 basis points, representing the smallest annual decline in eight months. This deceleration suggests that the sharp downward pressure on interest rates may be easing. The moderation in rate declines comes as Singapore continues to attract capital inflows, with foreign exchange reserves rising 10% year-on-year in Feb 2026, reinforcing the city-state's position as a regional safe haven. Meanwhile, Hong Kong's 3-month Hong Kong Interbank Offered Rate (3M-HIBOR) declined 18 basis points month-on-month to 2.69% in Feb, continuing its fourth consecutive month of decreases. Banking Performance Reflects Sector Headwinds Singapore's major banks reported fourth-quarter 2025 earnings that fell slightly below market expectations, with overall earnings declining 5% year-on-year. This performance was primarily driven by a 5% decrease in net interest income as net interest margins compressed by 22 basis points year-on-year. However, robust fee income growth of 13% helped partially offset the decline in traditional lending income. The banking sector has shown resilience through improved deposit dynamics. Current Account and Savings Account (CASA) balances rose 12% year-on-year, whilst the CASA ratio to total deposits increased to 19.8% in Dec 2025 from 19.6% previously. This improvement in low-cost funding provides banks with a cushion against margin compression and helps lower overall funding costs. Outlook and Investment Stance Phillip Securities Research maintains a NEUTRAL stance on the Singapore banking sector, acknowledging both challenges and opportunities ahead. The research house expects fiscal year 2026 profit after tax and minority interests to increase by 7% year-on-year, supported by continued fee income growth despite ongoing pressure on net interest income. Banks are providing guidance for low to mid-single digit loan growth, with Singapore loan growth continuing to climb at 6.1% as of Jan 2026. Management teams across the sector indicate that net interest margin compression should begin to ease in fiscal year 2026 as deposit rate cuts flow through and interest rates stabilise. The research highlights that increased market volatility and higher Singapore Dollar Average Volume are boosting capital markets and fee income, helping to offset traditional banking headwinds. Additionally, rising oil prices present inflation risks that could potentially delay further rate cuts, providing some support for margins. Despite asset quality concerns at United Overseas Bank, analysts view the bank's pre-emptive provisioning approach as prudent, with overall sector risks considered contained. All three major Singapore banks have committed to completing their previously announced capital return programmes, whilst dividend yields remain attractive at 5.1% with ongoing share buybacks improving return on equity. Frequently Asked Questions Q: How did Singapore banks perform in the fourth quarter of 2025? A: Fourth-quarter 2025 bank earnings were slightly below expectations, with earnings declining 5% year-on-year primarily due to lower net interest income, though this was partially offset by 13% growth in fee income. Q: What is the outlook for net interest margins in 2026? A: Banks are guiding that net interest margin compression should ease in fiscal year 2026 as deposit rate cuts begin to flow through and interest rates stabilise, following a 22 basis point year-on-year decline in the fourth quarter. Q: How are deposit trends supporting the banks? A: CASA balances rose 12% year-on-year with the CASA ratio to deposits improving to 19.8%, providing a tailwind for banks by lowering funding costs and cushioning net interest margin compression. Q: What factors could support banking margins going forward? A: Rising oil prices raise inflation risks that could potentially delay further rate cuts, whilst increased market volatility is boosting capital markets and fee income to help offset traditional banking headwinds. Q: What is the expected profit growth for Singapore banks in 2026? A: Phillip Securities Research expects fiscal year 2026 profit after tax and minority interests to increase by 7% year-on-year, as fee income growth will be partially offset by declining net interest income. Q: What are the key risks facing the banking sector? A: The main challenges include continued net interest margin compression from declining interest rates and asset quality concerns, though overall risks are viewed as contained with banks taking prudent provisioning approaches. Q: How attractive are Singapore bank dividends currently? A: Banks' dividend yields remain attractive at 5.1%, with all three major banks committed to completing their previously announced capital return plans and ongoing share buybacks improving return on equity. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Oiltek International Shows Resilient Performance Amid Order Book Challenges