Personal financial ratios

Table of Contents

Personal financial ratios

Although it can be an uphill battle, managing our personal finances is a crucial component of our life. Personal financial ratios serve as efficient tools that enable people to understand the state of their finances better. They provide individuals with an easy checklist to adhere to in order to make smart financial decisions, safeguard their future, and reach their financial objectives.

What are personal financial ratios?

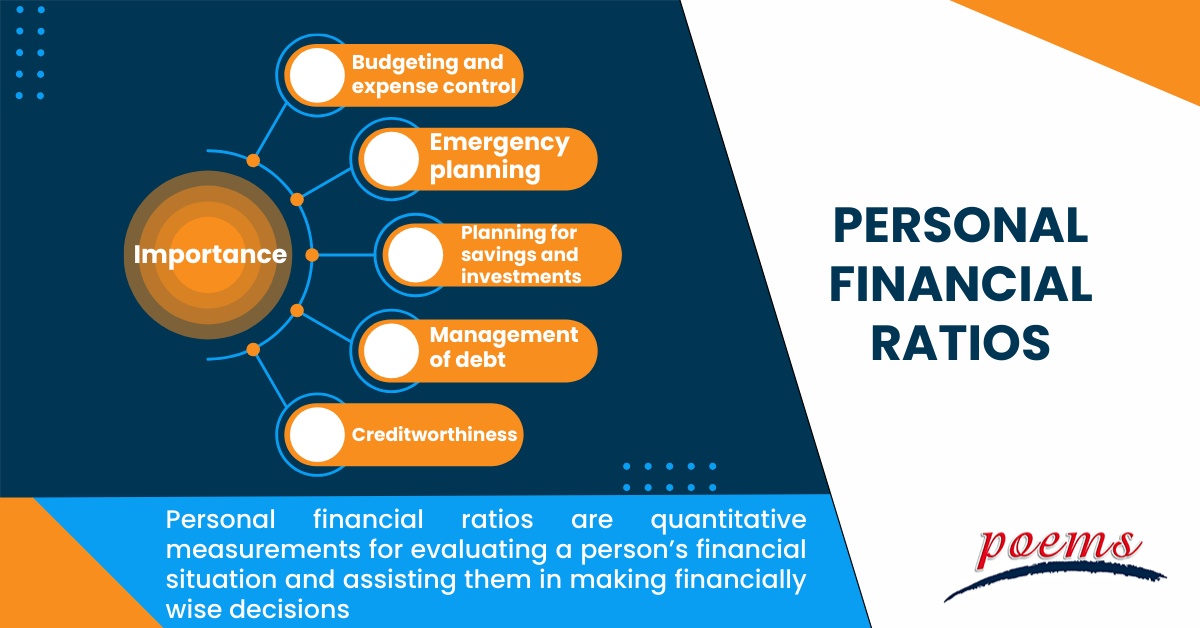

Personal financial ratios are quantitative measurements for evaluating a person’s financial situation and assisting them in making financially wise decisions. These ratios provide information on a person’s wealth in general, as well as their ability to manage debt and save money. These ratios assist people in assessing their financial security, setting objectives, and making necessary modifications to guarantee a safe and profitable financial future.

Understanding personal financial ratios

Personal financial ratios assist you in analysing how your income, spending, debt, and savings relate to one another and other aspects of your financial life. Regularly assessing these ratios will allow you to assess your financial stability and make necessary modifications to reach your financial objectives.

It’s important to comprehend what the ratios signify once you’ve calculated them:

- Healthy ratios

A DTI ratio of less than 36% is generally regarded as healthy. A net worth that is positive and has a savings ratio of at least 20% is optimal.

- Emergency fund ratio

Aim for an emergency fund ratio of 100% or more, which would mean you could pay for many months’ worth of costs without receiving any income.

- Liquidity ratio

A ratio that is higher than one indicates you have adequate liquid assets to satisfy your immediate obligations without taking on more debt.

- Investment ratio

To protect your retirement and long-term financial goals, strive for an investment ratio of at least 15% or higher.

Working of personal financial ratios

Personal finance ratios contrast important financial information to give an overview of one’s financial status. Here is how they work:

- Debt-to-income ratio

It calculates the portion of your income that is used to pay off debt. Since a lower DTI suggests greater discretionary income, it is an indication of improved financial health.

- Net worth

It is calculated by deducting all of your liabilities from all of your assets. It illustrates your total financial situation. The objective is to have a positive net worth, which shows that your assets outweigh your obligations.

- Investment ratio

This ratio indicates the proportion of your money you put toward long-term objectives like retirement. Your financial future is more secure when your investment ratio is larger.

- Emergency fund ratio

It evaluates how adequate your emergency funds are. It is usually advised to have three to six months’ worth of living costs in savings.

Importance of personal financial ratios

Personal financial ratios are essential tools that help individuals make well-informed decisions about their financial well-being and offer insightful information about their financial health. These ratios provide a comprehensive picture of a person’s financial state, enabling them to evaluate their present circumstances, set financial objectives, and create plans to reach those goals. Some of the key significance of these ratios include:

- Budgeting and expense control

The expense-to-income ratio and debt-to-income ratio are two ratios that assist people in keeping track of their expenditures and making sure they are living within their budgets. By doing so, you can avoid going into debt that you can’t afford.

- Emergency planning

Personal financial ratios can show how prepared a person is to deal with unforeseen expenditures. A safety net amid emergencies can be provided by a high liquidity ratio (such as savings or an emergency fund).

- Planning for savings and investments

Individuals can allocate funds for investing and saving thanks to ratios like the savings ratio and the investment-to-income ratio, which helps them accumulate wealth over time and reach long-term financial objectives.

- Management of debt

For controlling and lowering debt, ratios like the debt-to-income and debt-to-asset ratios are important. They serve as a reference when deciding how much debt is appropriate and when it’s time to settle current loans.

- Creditworthiness

Lenders frequently use personal financial ratios to evaluate creditworthiness. Improved borrowing conditions and interest rates may result from maintaining healthy ratios.

Examples of personal financial ratios

We can take the debt-to-income ratio as one example of a personal financial ratio. By comparing an individual’s overall debt with their total income, this ratio is applied to assessing his financial situation.

For example, if a person makes US$50,000 per year and has US$10,000 in debt, his debt-to-income ratio is 20%. Lenders can assess a person’s capacity to handle extra debt or credit using this information responsibly. A greater ratio might indicate financial challenges and lead to loan denials or higher interest rates. In contrast, a smaller ratio signals improved financial stability and indicates that the individual may be a more attractive candidate for loans or mortgages.

Frequently Asked Questions

Financial ratio analysis is classified into four types:

- Liquidity ratios

These measure a company’s capacity to satisfy immediate obligations and thereby assess its short-term financial sustainability.

- Profitability ratios

These assess a company’s capacity to create profits in relation to its assets, revenue, or equity.

- Solvency ratios

These measure a company’s long-term financial health and ability to fulfil its debt obligations.

- Efficiency ratios

These analyse how well a company uses its assets and runs its operations in order to create sales and profits.

- Key ratios consist of:

- Debt-to-Income ratio

It evaluates the percentage of debt to income and aids in determining borrowing capability.

- Savings rate ratio

It represents the percentage of income saved, which aids in the development of an emergency fund and long-term investments.

- Investment asset allocation ratio

For risk management and diversification, the investment asset allocation ratio distributes assets among various asset classes.

- The debt repayment ratio

It also keeps track of the debt reduction process.

Every company should monitor the following five financial ratios:

- Liquidity ratios

- Profitability ratio

- Efficiency ratios

- Market value ratios

- Leverage ratios

A good personal liquidity ratio is usually 20-30 %. The ability to meet short-term financial obligations with readily accessible cash or assets is measured by this ratio. Higher percentages indicate greater financial stability since it suggests a larger proportion of one’s assets may be quickly turned into cash to pay for emergencies, bills, or unforeseen obligations. The appropriate ratio, however, may change based on the situation.

Related Terms

- Cost of Equity

- Capital Adequacy Ratio (CAR)

- Interest Coverage Ratio

- Industry Groups

- Income Statement

- Historical Volatility (HV)

- Embedded Options

- Dynamic Asset Allocation

- Depositary Receipts

- Deferment Payment Option

- Debt-to-Equity Ratio

- Financial Futures

- Contingent Capital

- Conduit Issuers

- Calendar Spread

- Cost of Equity

- Capital Adequacy Ratio (CAR)

- Interest Coverage Ratio

- Industry Groups

- Income Statement

- Historical Volatility (HV)

- Embedded Options

- Dynamic Asset Allocation

- Depositary Receipts

- Deferment Payment Option

- Debt-to-Equity Ratio

- Financial Futures

- Contingent Capital

- Conduit Issuers

- Calendar Spread

- Devaluation

- Grading Certificates

- Distributable Net Income

- Cover Order

- Tracking Index

- Auction Rate Securities

- Arbitrage-Free Pricing

- Net Profits Interest

- Borrowing Limit

- Algorithmic Trading

- Corporate Action

- Spillover Effect

- Economic Forecasting

- Treynor Ratio

- Hammer Candlestick

- DuPont Analysis

- Net Profit Margin

- Law of One Price

- Annual Value

- Rollover option

- Financial Analysis

- Currency Hedging

- Lump sum payment

- Annual Percentage Yield (APY)

- Excess Equity

- Fiduciary Duty

- Bought-deal underwriting

- Anonymous Trading

- Fair Market Value

- Fixed Income Securities

- Redemption fee

- Acid Test Ratio

- Bid Ask price

- Finance Charge

- Futures

- Basis grades

- Short Covering

- Visible Supply

- Transferable notice

- Intangibles expenses

- Strong order book

- Fiat money

- Trailing Stops

- Exchange Control

- Relevant Cost

- Dow Theory

- Hyperdeflation

- Hope Credit

- Futures contracts

- Human capital

- Subrogation

- Qualifying Annuity

- Strategic Alliance

- Probate Court

- Procurement

- Holding company

- Harmonic mean

- Income protection insurance

- Recession

- Savings Ratios

- Pump and dump

- Total Debt Servicing Ratio

- Debt to Asset Ratio

- Liquid Assets to Net Worth Ratio

- Liquidity Ratio

- Payroll deduction plan

- Operating expenses

- Demand elasticity

- Deferred compensation

- Conflict theory

- Acid-test ratio

- Withholding Tax

- Benchmark index

- Double Taxation Relief

- Debtor Risk

- Securitization

- Yield on Distribution

- Currency Swap

- Overcollateralization

- Efficient Frontier

- Listing Rules

- Green Shoe Options

- Accrued Interest

- Market Order

- Accrued Expenses

- Target Leverage Ratio

- Acceptance Credit

- Balloon Interest

- Abridged Prospectus

- Data Tagging

- Perpetuity

- Optimal portfolio

- Hybrid annuity

- Investor fallout

- Intermediated market

- Information-less trades

- Back Months

- Adjusted Futures Price

- Expected maturity date

- Excess spread

- Quantitative tightening

- Accreted Value

- Equity Clawback

- Soft Dollar Broker

- Stagnation

- Replenishment

- Decoupling

- Holding period

- Regression analysis

- Wealth manager

- Financial plan

- Adequacy of coverage

- Actual market

- Credit risk

- Insurance

- Financial independence

- Annual report

- Financial management

- Ageing schedule

- Global indices

- Folio number

- Accrual basis

- Liquidity risk

- Quick Ratio

- Unearned Income

- Sustainability

- Value at Risk

- Vertical Financial Analysis

- Residual maturity

- Operating Margin

- Trust deed

- Profit and Loss Statement

- Junior Market

- Affinity fraud

- Base currency

- Working capital

- Individual Savings Account

- Redemption yield

- Net profit margin

- Fringe benefits

- Fiscal policy

- Escrow

- Externality

- Multi-level marketing

- Joint tenancy

- Liquidity coverage ratio

- Hurdle rate

- Kiddie tax

- Giffen Goods

- Keynesian economics

- EBITA

- Risk Tolerance

- Disbursement

- Bayes’ Theorem

- Amalgamation

- Adverse selection

- Contribution Margin

- Accounting Equation

- Value chain

- Gross Income

- Net present value

- Liability

- Leverage ratio

- Inventory turnover

- Gross margin

- Collateral

- Being Bearish

- Being Bullish

- Commodity

- Exchange rate

- Basis point

- Inception date

- Riskometer

- Trigger Option

- Zeta model

- Racketeering

- Market Indexes

- Short Selling

- Quartile rank

- Defeasance

- Cut-off-time

- Business-to-Consumer

- Bankruptcy

- Acquisition

- Turnover Ratio

- Indexation

- Fiduciary responsibility

- Benchmark

- Pegging

- Illiquidity

- Backwardation

- Backup Withholding

- Buyout

- Beneficial owner

- Contingent deferred sales charge

- Exchange privilege

- Asset allocation

- Maturity distribution

- Letter of Intent

- Emerging Markets

- Consensus Estimate

- Cash Settlement

- Cash Flow

- Capital Lease Obligations

- Book-to-Bill-Ratio

- Capital Gains or Losses

- Balance Sheet

- Capital Lease

Most Popular Terms

Other Terms

- Bond Convexity

- Compound Yield

- Brokerage Account

- Discretionary Accounts

- Industry Groups

- Growth Rate

- Green Bond Principles

- Gamma Scalping

- Funding Ratio

- Free-Float Methodology

- Foreign Direct Investment (FDI)

- Floating Dividend Rate

- Flight to Quality

- Real Return

- Protective Put

- Perpetual Bond

- Option Adjusted Spread (OAS)

- Non-Diversifiable Risk

- Merger Arbitrage

- Liability-Driven Investment (LDI)

- Income Bonds

- Guaranteed Investment Contract (GIC)

- Flash Crash

- Equity Carve-Outs

- Cost Basis

- Deferred Annuity

- Cash-on-Cash Return

- Earning Surprise

- Bubble

- Beta Risk

- Bear Spread

- Asset Play

- Accrued Market Discount

- Ladder Strategy

- Junk Status

- Intrinsic Value of Stock

- Interest-Only Bonds (IO)

- Inflation Hedge

- Incremental Yield

- Industrial Bonds

- Holding Period Return

- Hedge Effectiveness

- Flat Yield Curve

- Fallen Angel

- Exotic Options

- Execution Risk

- Exchange-Traded Notes

- Event-Driven Strategy

- Eurodollar Bonds

- Enhanced Index Fund

Know More about

Tools/Educational Resources

Markets Offered by POEMS

Read the Latest Market Journal

Raffles Medical Group Faces Challenging Operating Environment

Phillip Securities Research Maintains Neutral Stance with Reduced Target Price Raffles Medical Group Ltd, a Singapore-based healthcare services provider operating hospitals, medical centers, and transitional care facilities across Singapore and Greater China, is experiencing significant headwinds as lower-cost alternatives pressure its traditional business model. Phillip Securities Research has maintained its NEUTRAL recommendation while lowering the DCF target price to S$0.92 from the previous S$1.02. Disappointing Half-Year Performance The company's 1H26 results fell short of expectations, with revenue and adjusted profit after tax and minority interests (PATMI) representing only 44% and 40% of full-year estimates respectively. Adjusted PATMI declined 18% year-over-year to S$29 million, while revenue dropped 7% to S$353 million, primarily due to weakness in the transitional care facility segment. Healthcare services revenue contracted sharply by 17% year-over-year to S$112 million, driven by reduced patient load from TCF operations. The expansion of public hospital beds has significantly impacted TCF utilization rates, creating substantial operational challenges for this high-fixed-cost segment. Positive Developments Amid Challenges Despite the overall weak performance, Raffles Medical's hospital services demonstrated resilience with profit before tax growing 11% year-over-year to S$19.7 million in 1H26. This improvement stems from higher revenue intensity surgical cases and moderate price increases, indicating the company's ability to maintain margins in its core hospital operations through strategic pricing and case mix optimization. Significant Operational Headwinds The transitional care facility operations present the most significant drag on performance. While TCF contribution figures are not separately disclosed, the segment's high fixed costs in wages and rental expenses led to a dramatic 38% year-over-year plunge in earnings to S$15.6 million. The substantial fixed cost structure makes this segment particularly vulnerable to utilisation pressures from expanded public hospital capacity. Outlook and Strategic Challenges Phillip Securities Research has reduced FY26e adjusted PATMI estimates by 10% to S$65.4 million, reflecting 5% lower revenue projections. The challenging operating environment persists as patient volumes face pressure from cheaper alternatives in overseas markets, particularly Malaysia, and expanded public hospital options. Additionally, private insurers continue pressuring revenue intensity improvements, while China operations show growth potential despite ongoing regulatory uncertainties. [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Frasers Centrepoint Trust Maintains Strong Position Despite Minor Operational Adjustments

Frasers Centrepoint Trust (FCT), a prominent retail real estate investment trust focused on suburban shopping malls, continues to demonstrate resilience in its operational performance while actively recycling capital for future growth opportunities. The trust's portfolio centres on defensive sub-urban mall assets anchored by essential services, positioning it well to weather global economic uncertainties. Operational Performance Shows Stability In its third quarter 2026 business update, FCT reported a marginal decline in retail portfolio occupancy of 20 basis points quarter-over-quarter to 99.6%, primarily attributed to tenant churn as the trust optimised its tenant mix. Despite this slight adjustment, shopper traffic demonstrated positive momentum with a 2.4% year-over-year increase. However, tenants' sales growth remained modest at 0.2% year-over-year, reflecting the ongoing impact of tenancy churn and tenant refresh initiatives across the portfolio. Strategic Capital Recycling Initiatives FCT is executing a significant capital recycling strategy through the divestment of White Sands, its smallest mall, for S$467 million. This transaction represents an 8.4% premium to valuation and delivers a 4.6% exit yield. Simultaneously, the trust is expanding its development capabilities by acquiring a 50% stake in the retail component of the Bayshore Drive integrated development. This project encompasses approximately 170,000 square feet of retail net lettable area with a total cost of S$613 million on a 100% basis. Strong Financial Foundation Supports Growth The trust's financial position remains robust, with several positive indicators supporting its outlook. Portfolio occupancy maintained a healthy level at 99.6% in the third quarter, with year-to-date welcoming of 69 new-to-portfolio tenants enhancing the overall tenant mix quality. The financial structure has improved significantly, with the average all-in cost of debt declining 20 basis points quarter-over-quarter to 3% following the expiry of higher-cost interest rate swaps. Currently, 65.7% of borrowings are hedged to fixed rates, providing stability against interest rate fluctuations. Aggregate leverage stands at 40.4% but is projected to decrease to 36.5% upon completion of the White Sands divestment. The debt maturity profile remains favorable, with no debt maturing in FY26 and only 4% of borrowings requiring refinancing in FY27. Investment Outlook Phillip Securities Research maintains a BUY recommendation with an unchanged target price of S$2.70, citing no negatives in their assessment. The Bayshore development is expected to deliver a 5% yield on cost upon completion by end-2030, potentially increasing distributable income by approximately 3% upon stabilisation. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Company Overview Alphabet Inc. (GOOGL) operates as a technology conglomerate primarily through its Google subsidiary, focusing on internet search, online advertising, cloud computing services, and artificial intelligence solutions. The company's core business segments include Search, YouTube advertising, and Google Cloud, serving both consumer and enterprise markets globally. Strong Financial Performance Driven by AI Integration Alphabet delivered robust second-quarter 2026 results, with adjusted profit after tax and minority interest growing 24% year-on-year to US$35 billion. Revenue increased 24% to US$119.8 billion, representing 45% of full-year forecasts for revenue and 42% for profit, reflecting typical seasonal patterns in the advertising segment. The company's performance was underpinned by resilient advertising growth of 14% year-on-year, enhanced by Gemini integration across Search platforms and improved monetisation of YouTube Shorts and connected television offerings. Additionally, the fastest cloud growth on record, surging 82% year-on-year, demonstrated strong enterprise demand for AI products and services. Record Cloud Segment Expansion Google Cloud emerged as the standout performer, with revenue accelerating to US$24.8 billion in the second quarter, compared to 32% growth in the prior year period. This exceptional growth was driven by robust demand for Enterprise AI products and services, with nearly 90% of Fortune 100 companies adopting Gemini Enterprise solutions. Operating margins in the Cloud segment expanded significantly to 35.6% from 20.7% in the previous year, reflecting improved operational leverage. The Cloud backlog grew 3.8 times year-on-year to US$514 billion, with management expecting approximately 50% recognition as revenue over the next 24 months. To address supply constraints, Alphabet plans to increase third-party compute capacity usage from the third quarter onwards. AI-Enhanced Advertising Performance Search revenue demonstrated strong momentum, increasing 17% year-on-year to US$63.3 billion, with retail and finance sectors providing the largest contributions. YouTube advertising revenue rose 13% to US$11.1 billion, supported by continued Shorts and connected TV growth. The FIFA World Cup 2026 provided additional tailwinds, driving record Search usage and YouTube's highest viewership as an official broadcast partner. AI Mode inference costs have declined to their lowest levels since the 2025 launch, indicating improving monetisation efficiency. Paid clicks grew 13% year-on-year, marking three consecutive quarters of double-digit growth and suggesting successful Gemini integration. Investment Outlook and Rating Phillip Securities Research upgraded Alphabet to a BUY rating whilst lowering the DCF target price to US$425 from US$450. The firm reduced FY26 revenue and profit forecasts by approximately 2% and 4% respectively, reflecting moderate margin expansion amid ongoing supply chain constraints. Despite temporary free cash flow pressure from heavy AI investments, analysts remain constructive on the long-term outlook. Alphabet's vertically integrated AI ecosystem, spanning custom silicon, optimised data centres, and high-performing Gemini models, should continue supporting robust growth across advertising and cloud businesses. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Company Overview Keppel DC REIT is a Singapore-listed real estate investment trust that owns and operates a diversified portfolio of data centres across key markets. The REIT focuses on providing mission-critical infrastructure to support the growing digital economy, with properties spanning multiple geographical regions including Asia-Pacific and Europe. Strong Half-Year Performance Driven by Strategic Acquisitions Keppel DC REIT delivered impressive results in the first half of FY26, with distribution per unit (DPU) reaching 5.71 Singapore cents, representing an 11.3% year-on-year increase. This performance was in line with analyst expectations and constituted 52% of the full-year forecast. The growth was primarily attributed to the accretive acquisition of Tokyo Data Centre 3, combined with positive rental reversions and escalations across the portfolio. However, these gains were partially offset by the divestment of Kelsterbach Data Centre. Distribution income increased by 18.5% year-on-year, outpacing DPU growth due to an expanded unit base following equity fund raisings to finance recent acquisitions. Rental Market Dynamics and Portfolio Performance The REIT maintained healthy rental reversions at 10% during the first half, though second-quarter reversions moderated to approximately 5% compared to the exceptional 51% recorded in the first quarter. Looking ahead, rental reversions in the second half are expected to be higher, supported by the Gore Hill Data Centre lease renewal where rents more than doubled and will contribute from the third quarter onwards. Portfolio occupancy declined to 92.5% from 95.6% in the first quarter due to the expiry of the Cardiff Data Centre contract. Despite this decrease, the earnings impact should be limited as 95% of revenue-generating power capacity remains contracted. Financial Strength and Growth Prospects The REIT maintains a robust balance sheet with ample debt headroom for future acquisitions. Aggregate leverage improved by 110 basis points quarter-on-quarter to 34% following repayment of the consumption tax loan for Tokyo Data Centre 3, leaving approximately S$673 million of debt headroom against its 40% internal cap. The average cost of debt increased marginally by 10 basis points to 2.7%, with forecasted foreign-sourced distributions substantially hedged through the first half of FY27. Analysts maintain an ACCUMULATE rating with a raised target price of S$2.46, up from S$2.37, reflecting higher rental assumptions and continued NetCo Bonds contribution. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Company Overview OUE REIT is a Singapore-listed real estate investment trust with a diversified portfolio spanning hospitality and commercial properties. The REIT operates prominent hospitality assets including Hilton Singapore Orchard and Crowne Plaza Changi Airport, alongside commercial properties such as OUE Downtown and maintains a stake in Salesforce Tower. Strong First Half Performance Driven by Hospitality Sector OUE REIT delivered robust first-half 2026 results, with gross revenue and net property income rising 3.8% and 4.8% year-on-year to S$136.1 million and S$110.3 million respectively, representing 50% and 51% of full-year forecasts. Distribution per unit surged 28.6% year-on-year to 1.26 cents, exceeding expectations and forming 55% of the full-year forecast. The standout performer was the hospitality segment, which demonstrated remarkable resilience and growth momentum. Revenue increased 11.2% year-on-year to S$50.1 million, whilst net property income climbed 12.3% to S$45.1 million. The segment's revenue per available room rose 10.7% to S$258, driven by strategic commercial execution and operational improvements. Key Positive Drivers The hospitality segment's strong performance reflects proactive management initiatives and market positioning. Hilton Singapore Orchard achieved a 12.6% year-on-year RevPAR increase through successful corporate account acquisitions and higher occupancy rates. The property's positioning as a premium US corporate brand enabled it to capture rising American corporate demand, which increased approximately 4% year-on-year, offsetting softer tourist arrivals from Indonesia and China. Crowne Plaza Changi Airport contributed with a 7.5% year-on-year RevPAR improvement, benefiting from increased transit passenger volumes despite a 1.7% decline in international passenger numbers during the period. Financial costs provided additional support, declining 16.6% year-on-year to S$37.8 million. The average cost of debt improved from 4.2% to 3.6%, whilst interest coverage strengthened to 2.8 times from 2.6 times previously. Investment Outlook and Recommendation Phillip Securities Research maintains a BUY recommendation with an unchanged dividend discount model-based target price of S$0.45. The REIT trades at a forward dividend yield of 6.2% and price-to-net asset value of 0.57 times. Expected catalysts include accretive redeployment of divestment proceeds into Salesforce Tower, successful backfilling of Deloitte's 150,000 square feet space at OUE Downtown at market rents, and continued cost savings from refinancing S$400 million of debt maturities due in 2027. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Company Overview SIA Engineering Co. Ltd (SIAEC) is a leading aircraft maintenance, repair and overhaul (MRO) service provider operating across the Asia-Pacific region. The company provides comprehensive maintenance services including airframe and line maintenance, engine and component services, with operations spanning Singapore, Malaysia, Cambodia, the Philippines, India, and recently China through strategic joint ventures. First Quarter Performance Analysis SIAEC reported a 6.1% year-on-year decline in first quarter FY27 profit after tax and minority interests to S$40.3 million, representing 22% of the full year estimate. The earnings decline was primarily attributed to a S$7 million reduction in share of profits from the engine and component segment, driven by higher investment costs associated with the SAESL joint venture. Associates and joint venture income fell 18% year-on-year to S$31 million, with the engine and component segment declining 19.2% due to elevated investment costs. However, this was partially offset by the airframe and line maintenance segment, which posted a 14.3% year-on-year increase driven by growth in flight handling volume, which rose 2.9% year-on-year. Core Business Resilience Evident Despite the headline revenue decline of 8.6% year-on-year to S$327.6 million, the underlying business fundamentals remain intact. The revenue drop was attributed to the scope and work content performed during the quarter, with lower materials-related work being conducted. Heavy checks performed decreased 13% to 20 checks, whilst managed fleet size for components revenue fell 9% to 151 aircraft, indicating reduced parts-intensive work during the period. Importantly, operating profit surged 159% due to lower material costs and reduced outsourced repair costs. Ex-materials revenue grew 4.2% year-on-year, demonstrating that direct labour-related revenue increased, with line maintenance operations handling 2.9% more flights year-on-year to 40,615 flights. Strategic Positioning and Outlook Phillip Securities Research maintains its BUY recommendation with an unchanged target price of S$4.06. The research house highlights SIAEC's strengthening position in the Indian MRO market through Air India partnerships, regional maintenance capacity expansion across Southeast Asia, and market entry into China via the Arport AME joint venture. These strategic initiatives position the group to capture growing APAC MRO demand. Investment costs at SAESL are expected to peak during the current financial year. The stock trades at a FY27 estimated price-to-earnings ratio of 19.9 times. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Singapore REITs Poised for DPU Growth in First Half 2026 Amid Lower Interest Rates

Market Performance and Outlook Singapore Real Estate Investment Trusts (S-REITs) demonstrated modest resilience in June 2026, with the S-REITs Index gaining 0.4% following May's 1.6% decline. The sector is positioned for stronger performance ahead, with analysts expecting approximately 3% year-on-year distribution per unit (DPU) growth for the second quarter of 2026, driven by improved net property income from higher rents and reduced financing costs in a lower interest rate environment. Sector Dynamics and Interest Rate Environment The average cost of debt for S-REITs has declined by approximately 40 basis points year-on-year as of end-March 2026, with expectations of a further 10 basis points reduction throughout the remainder of the year. This improvement is supported by refinancing opportunities at lower Singapore Dollar benchmark rates, particularly benefiting REITs with substantial SGD-denominated debt portfolios. The 3-month Singapore Overnight Rate Average (SORA) has stabilised around 1.1%, remaining approximately 100 basis points below levels from a year ago. However, overseas interest rates have begun to edge higher amid expectations of renewed inflationary pressures from the ongoing Middle East conflict. The Reserve Bank of Australia, European Central Bank, and Bank of Japan have all raised policy rates this year, suggesting that borrowing costs for foreign currency-denominated debt will gradually increase, though existing interest rate hedges should cushion the impact. Sectoral Performance and Investment Strategy The diversified REIT sub-sector led performance in June with a 3% gain, while the overseas commercial REIT sub-sector declined 6.5%. Retail, office, and industrial REITs are expected to continue delivering mid- to high-single-digit rental reversions, though hospitality REITs face softer operating performance due to higher airfares and travel disruptions from Middle East conflicts. Analysts maintain an overweight stance on S-REITs whilst remaining selective, favouring REITs with robust balance sheets, defensive earnings profiles, and higher proportions of fixed-rate debt to limit interest rate volatility exposure. Retail S-REITs remain preferred, supported by healthy tenant sales and limited new supply, which should underpin mid- to high-single-digit rental reversions in 2026. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Strong First Half Performance Driven by Singapore Assets Suntec REIT delivered robust first-half results with distributable per unit (DPU) of 3.936 Singapore cents, representing a substantial 24.8% year-on-year increase. This performance aligned with analyst expectations and constituted 52% of the full-year forecast. The growth was primarily attributed to an S$9.4 million (11.6%) reduction in finance costs and enhanced contributions from the Singapore office and retail portfolios. Company Overview Suntec REIT is a Singapore-based real estate investment trust that owns and manages a diversified portfolio of office, retail, and convention properties. The trust's flagship assets include Suntec City, Marina Bay Financial Centre properties, and overseas holdings including The Minster Building and 55 Currie Street. Singapore Portfolio Maintains Near-Full Occupancy The core Singapore operations demonstrated exceptional resilience, with both office and retail portfolios achieving near-full occupancy rates of 99.5%. The office portfolio recorded strong positive rental reversions of 10.1%, whilst the retail segment achieved even stronger rental growth of 10.7% during the first half. Analysts expect healthy rental reversions to continue, forecasting 5% for the office portfolio and 10% for retail in the full year. Key Positive Drivers The Singapore operations remain the primary earnings driver, with office occupancy rising 0.7 percentage points quarter-on-quarter to 99.5%. This strong performance is supported by limited core CBD supply and tight market vacancy, with demand coming from financial services and technology sectors. The retail segment benefited from major events including the F1 Singapore Grand Prix and BTS concert, which supported tenant sales growth of 7% in the first half. Tenant sales growth was primarily driven by food and beverage outlets, whilst discretionary retail remained resilient. Suntec Convention is expected to maintain stable performance with a healthy MICE pipeline providing support despite Middle East conflict uncertainties. Financial Position and Outlook Aggregate leverage increased to 43.0% from 41.6% following the redemption of S$150 million in perpetual securities. Phillip Securities Research maintains an ACCUMULATE recommendation with a raised target price of S$1.69, up from the previous S$1.63. The trust currently trades at an FY26e dividend yield of 5.45% and price-to-NAV of 0.72x. Frequently Asked Questions [market_journal_faq] This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.