Yield curve

Table of Contents

- Yield curve

- What is a yield curve?

- Understanding the yield curve

- How does the yield curve work?

- Types of yield curves

- Importance of yield curves

- How can investors use the yield curve?

- What is yield curve risk?

- What are yield curve theories?

- What is the relationship between the price of a bond and its yield?

- What is the difference between interest rates and bond yields?

Yield curve

Investments and debt are not created equally. They have various maturities and interest rates. The concept of yield curves is crucial to understanding them if you have invested outside your business or borrowed money. A yield curve can help you better understand the overall economy in which your company works and demonstrate how hard your investment is working for you.

Understanding yield curves is essential for comprehending how various interest rates operate and change over time. This is something that will be useful to your business and financial well-being. And they can aid in understanding an investment’s risk, possible returns, and even broader economic results.

What is a yield curve?

The interest rates on debt for different maturities are represented graphically by the yield curve. It shows the anticipated rate of return on an investor’s investment for a given time frame.

A bond’s yield is displayed on the graph’s vertical axis, while its remaining maturity time is displayed across the graph’s horizontal axis. Although the curve is normally upward-sloping, it may take on different shapes during different economic cycles.

Since long-term returns are lower than short-term returns, the yield curve can serve as a leading economic indicator, particularly when it flips to an inverted shape, which denotes an economic slump.

Understanding the yield curve

Understanding yield curves can help you and your organization in various ways. You can time a business or personal borrowing to coincide with favorably low rates by using it to assist you in forecasting interest rates.

Financial intermediaries may find it useful in understanding and anticipating their profits. Additionally, it can provide a more comprehensive view of the market and assist you in avoiding overpriced stocks that are less likely to increase the value of your investment portfolio.

How does the yield curve work?

A yield curve can easily show the bond market at a certain time. The average yields on bonds with short, medium, or long maturities from a certain trading day or week are often shown.

A yield curve uses a graph to show how much interest is paid on debt. Seeing each bond’s risk and potential return is a fantastic method. The vertical axis represents the bond’s yield or interest rate (expressed as a percentage), and the horizontal axis represents the term to maturity. The yield curve concept is most frequently used when looking at national treasury securities. It can be compared to another person, company, and mortgage lending rates.

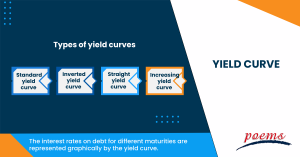

Types of yield curves

The types of yield curves are as follows:

- Standard yield curve

A typical yield curve slopes to the right as yields increase with maturity. This suggests that the market environment and the economy are sound and operating normally.

- Inverted yield curve

The yield curve is inverted when rates for shorter-term maturities are greater than those for longer-term maturities. The yield curve, in this instance, slopes rightward and downward instead of upward. This is a sign of a bear market or recession when bond prices and yields experience significant drops.

- Straight yield curve

A flat yield curve results when the yields for shorter- and longer-term maturities are almost equal. Mid-term maturities usually have a higher product than short-term or long-term maturities in the elevated zone in the middle of flat yield curves. The yield curve indicates this with a hump.

- Increasing yield curve

A steep yield curve has a steeper slope than a normal yield curve. The market environment is the same for steep and typical yield curves. But when the curve gets more vertical, the gap between short- and long-term rates grows, suggesting that investors believe that more favorable market circumstances will last longer.

Importance of yield curves

The importance of yield curves is as follows:

- Making interest rate predictions

Investors can understand the expected future trajectory of interest rates based on the curve’s form. In contrast to an inverted curve, which indicates short-term assets have a higher yield, a regular upward-sloping curve means long-term securities have a higher yield.

- The maturity and yield trade-off

The yield curve demonstrates the trade-off between yield and maturity. If the yield curve is upward sloping, the investor will have to take on greater risk by investing in longer-term securities to raise his yield.

- Securities that are overpriced or underpriced.

Investors can use the curve to determine if a security is now overpriced or underpriced. A security is underpriced or overpriced depending on where its rate of return falls on the yield curve. If it is above the yield curve, the deposit is underpriced.

- Benefits for financial intermediaries

The majority of the money that banks and other financial intermediaries use to lend is borrowed through selling short-term deposits. The greater the difference between lending and borrowing rates and the steeper the upward-sloping slope, the greater their profit. On the other hand, a flat or downward-sloping curve often indicates a decline in the earnings of financial intermediaries.

How can investors use the yield curve?

Investors can understand the expected future trajectory of interest rates based on the curve’s form. In contrast to an inverted curve, which indicates short-term assets have a higher yield, a regular upward-sloping curve means long-term securities have a higher yield.

What is yield curve risk?

The risk of an unfavorable change in market interest rates that comes with investing in fixed-income instruments is known as the yield curve risk. A change in market yields will affect a fixed-income instrument’s pricing.

What are yield curve theories?

According to the Yield Curve theory, a long-term bond’s interest rate will equal the average of the short-term interest rates anticipated to be in effect during the bond’s lifetime plus a term premium. Due to their risk aversion and distaste for the possibility of significant capital losses on long-term debt, investors want such a premium.

What is the relationship between the price of a bond and its yield?

Bond prices and yields have a significant but opposing link. Bond yields are higher than coupon rates when the bond price is less than the bond’s face value. Bond yields are lower than coupon rates when the bond price exceeds the bond’s face value.

What is the difference between interest rates and bond yields?

While a bond’s interest rates are determined based on the asset’s face value, bond yield is determined based on the value of your investment (which is the amount of money promised to a bondholder when the bond matures).

Related Terms

- Compound Yield

- Discretionary Accounts

- Industry Groups

- Growth Rate

- Foreign Direct Investment (FDI)

- Floating Dividend Rate

- Real Return

- Non-Diversifiable Risk

- Liability-Driven Investment (LDI)

- Guaranteed Investment Contract (GIC)

- Flash Crash

- Cost Basis

- Deferred Annuity

- Cash-on-Cash Return

- Bubble

- Compound Yield

- Discretionary Accounts

- Industry Groups

- Growth Rate

- Foreign Direct Investment (FDI)

- Floating Dividend Rate

- Real Return

- Non-Diversifiable Risk

- Liability-Driven Investment (LDI)

- Guaranteed Investment Contract (GIC)

- Flash Crash

- Cost Basis

- Deferred Annuity

- Cash-on-Cash Return

- Bubble

- Asset Play

- Accrued Market Discount

- Inflation Hedge

- Incremental Yield

- Holding Period Return

- Hedge Effectiveness

- Fallen Angel

- EBITDA Margin

- Dollar Rolls

- Dividend Declaration Date

- Distribution Yield

- Derivative Security

- Fiduciary

- Current Yield

- Core Position

- Cash Dividend

- Broken Date

- Share Classes

- Valuation Point

- Breadth Thrust Indicator

- Book-Entry Security

- Bearish Engulfing

- Core inflation

- Approvеd Invеstmеnts

- Allotment

- Annual Earnings Growth

- Solvency

- Impersonators

- Reinvestment date

- Volatile Market

- Trustee

- Sum-of-the-Parts Valuation (SOTP)

- Proxy Voting

- Passive Income

- Diversifying Portfolio

- Open-ended scheme

- Capital Gains Distribution

- Investment Insights

- Discounted Cash Flow (DCF)

- Portfolio manager

- Net assets

- Nominal Return

- Systematic Investment Plan

- Issuer Risk

- Fundamental Analysis

- Account Equity

- Withdrawal

- Realised Profit/Loss

- Unrealised Profit/Loss

- Negotiable Certificates of Deposit

- High-Quality Securities

- Shareholder Yield

- Conversion Privilege

- Cash Reserve

- Factor Investing

- Open-Ended Investment Company

- Front-End Load

- Tracking Error

- Replication

- Real Yield

- DSPP

- Bought Deal

- Bulletin Board System

- Portfolio turnover rate

- Reinvestment privilege

- Initial purchase

- Subsequent Purchase

- Fund Manager

- Target Price

- Top Holdings

- Liquidation

- Direct market access

- Deficit interest

- EPS forecast

- Adjusted distributed income

- International securities exchanges

- Margin Requirement

- Pledged Asset

- Stochastic Oscillator

- Prepayment risk

- Homemade leverage

- Prime bank investments

- ESG

- Capitulation

- Shareholder service fees

- Insurable Interest

- Minority Interest

- Passive Investing

- Market cycle

- Progressive tax

- Correlation

- NFT

- Carbon credits

- Hyperinflation

- Hostile takeover

- Travel insurance

- Money market

- Dividend investing

- Digital Assets

- Coupon yield

- Counterparty

- Sharpe ratio

- Alpha and beta

- Investment advisory

- Wealth management

- Variable annuity

- Asset management

- Value of Land

- Investment Policy

- Investment Horizon

- Forward Contracts

- Equity Hedging

- Encumbrance

- Money Market Instruments

- Share Market

- Opening price

- Transfer of Shares

- Alternative investments

- Lumpsum

- Derivatives market

- Operating assets

- Hypothecation

- Accumulated dividend

- Assets under management

- Endowment

- Return on investment

- Investments

- Acceleration clause

- Heat maps

- Lock-in period

- Tranches

- Stock Keeping Unit

- Real Estate Investment Trusts

- Prospectus

- Turnover

- Tangible assets

- Preference Shares

- Open-ended investment company

- Ordinary Shares

- Leverage

- Standard deviation

- Independent financial adviser

- ESG investing

- Earnest Money

- Primary market

- Leveraged Loan

- Transferring assets

- Shares

- Fixed annuity

- Underlying asset

- Quick asset

- Portfolio

- Mutual fund

- Xenocurrency

- Bitcoin Mining

- Option contract

- Depreciation

- Inflation

- Cryptocurrency

- Options

- Fixed income

- Asset

- Reinvestment option

- Capital appreciation

- Style Box

- Top-down Investing

- Trail commission

- Unit holder

- Rebalancing

- Vesting

- Private equity

- Bull Market

- Absolute Return

- Leaseback

- Impact investing

- Venture Capital

- Buy limit

- Asset stripper

- Volatility

- Investment objective

- Annuity

- Sustainable investing

- Face-amount certificate

- Lipper ratings

- Investment stewardship

- Average accounting return

- Asset class

- Active management

- Breakpoint

- Expense ratio

- Bear market

- Hedging

- Equity options

- Dollar-Cost Averaging (DCA)

- Due Diligence

- Contrarian Investor

Most Popular Terms

Other Terms

- Bond Convexity

- Brokerage Account

- Green Bond Principles

- Gamma Scalping

- Funding Ratio

- Free-Float Methodology

- Flight to Quality

- Protective Put

- Perpetual Bond

- Option Adjusted Spread (OAS)

- Merger Arbitrage

- Income Bonds

- Equity Carve-Outs

- Cost of Equity

- Earning Surprise

- Capital Adequacy Ratio (CAR)

- Beta Risk

- Bear Spread

- Ladder Strategy

- Junk Status

- Intrinsic Value of Stock

- Interest-Only Bonds (IO)

- Interest Coverage Ratio

- Industry Groups

- Industrial Bonds

- Income Statement

- Historical Volatility (HV)

- Flat Yield Curve

- Exotic Options

- Execution Risk

- Exchange-Traded Notes

- Event-Driven Strategy

- Eurodollar Bonds

- Enhanced Index Fund

- Embedded Options

- Dynamic Asset Allocation

- Dual-Currency Bond

- Downside Capture Ratio

- Dividend Capture Strategy

- Depositary Receipts

- Delta Neutral

- Deferment Payment Option

- Dark Pools

- Death Cross

- Debt-to-Equity Ratio

- Fixed-to-floating rate bonds

- First Call Date

- Financial Futures

- Firm Order

- Credit Default Swap (CDS)

Know More about

Tools/Educational Resources

Markets Offered by POEMS

Read the Latest Market Journal

Wee Hur Holdings Upgraded to Buy on Strong Performance and Growth Prospects

Company Overview Wee Hur Holdings Ltd is a Singapore-based company operating across three key business segments: worker dormitory operations, building construction, and property development. The company has established itself as a significant player in Singapore's infrastructure and accommodation sectors, with substantial dormitory assets and a growing construction order book. Strong Financial Performance Drives Upgrade Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, raising the target price to S$1.08 from S$0.90 previously. This upgrade follows exceptional 2H25 results that significantly exceeded expectations, with revenue and adjusted PATMI reaching 114% and 138% of full-year forecasts respectively. The company's adjusted PATMI surged 81% year-on-year to S$50 million in 2H25, driven by multiple growth catalysts across its business segments. The strong performance reflects successful execution of the company's diversified business model and strategic positioning in Singapore's infrastructure development. Worker Dormitory Business Anchors Growth The worker dormitory segment delivered robust performance, with Tuas View Dormitory achieving 95% occupancy compared to 93% in FY24, alongside positive rental revisions of approximately 5% year-on-year. The segment benefited significantly from Pioneer Lodge's Phase 1 operations, which added 3,088 beds representing a 20% capacity increase since May 2025. This expansion drove dormitory revenue up 21% year-on-year to S$50.8 million in 2H25. Pioneer Lodge's Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to contribute to occupancy ramp-up in FY26. Construction Segment Shows Marked Improvement The building construction segment demonstrated remarkable turnaround, with revenue spiking 172% year-on-year to S$50 million in 2H25. Operating margins improved substantially by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24. This improvement was driven by higher recognition of external projects, which now comprise 99% of the company's S$673 million order book, up from 59% previously. The expanded order book, growing from S$263 million in FY24, is expected to support construction segment growth through 4Q29. Strategic Portfolio Adjustments The research firm's sum-of-the-parts valuation model reflects strategic portfolio changes, including the removal of Mega@Woodlands property development and the addition of Wee Hur's 50% stake in the S$614 million Upper Thomson Road GLS site. The model also incorporates the company's estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III, backed by a 708-bed Australia PBSA. Future Outlook With major construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort on the horizon, analysts expect Wee Hur's 15,744-bed Tuas View Dormitory lease to be extended beyond November 2026, providing continued revenue visibility for the dormitory business. Frequently Asked Questions Q: What is Phillip Securities Research's current recommendation and target price for Wee Hur Holdings? A: Phillip Securities Research has upgraded Wee Hur Holdings to BUY from NEUTRAL, with a higher target price of S$1.08, increased from the previous target of S$0.90. Q: How did Wee Hur's 2H25 results compare to expectations? A: The company's 2H25 revenue and adjusted PATMI significantly exceeded expectations, reaching 114% and 138% of full-year forecasts respectively, with adjusted PATMI surging 81% year-on-year to S$50 million. Q: What drove the strong performance in the worker dormitory segment? A: The dormitory segment benefited from Tuas View Dormitory's improved occupancy rate of 95% and positive rental revisions of about 5% year-on-year, plus contributions from Pioneer Lodge Phase 1's additional 3,088 beds, driving dormitory revenue up 21% year-on-year to S$50.8 million. Q: How has the building construction segment's profitability changed? A: The building construction segment's operating margins improved significantly by 10 percentage points year-on-year to -7% in FY25, compared to -17% in FY24, driven by higher recognition of external projects and an expanded order book. Q: What is the current size and composition of Wee Hur's construction order book? A: The company's construction order book stands at S$673 million, up from S$263 million in FY24, with external projects now comprising 99% of the order book compared to 59% previously. This order book is expected to support growth through 4Q29. Q: When will Pioneer Lodge Phase 2 contribute to operations? A: Pioneer Lodge Phase 2, comprising 7,412 beds and representing a 39% capacity increase, received its temporary occupancy permit in 4Q25 and is expected to ramp up occupancy in FY26. Q: What major construction projects could benefit Wee Hur's dormitory business? A: Major upcoming construction projects including Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort are expected to support the extension of Wee Hur's 15,744-bed Tuas View Dormitory lease beyond November 2026. Q: What changes were made to the valuation model? A: The sum-of-the-parts model removed Mega@Woodlands property development and included Wee Hur's 50% stake in the S$614 million Upper Thomson Road GLS site, plus the company's estimated 20% stake in the 344-key DoubleTree by Hilton hotel and Fund III backed by a 708-bed Australia PBSA. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

TeleChoice International Ltd Maintains Growth Trajectory with Strong FY25 Performance

Company Overview TeleChoice International Ltd is a telecommunications services provider focused on personal communications systems (PCS) and network engineering services. The company operates across Southeast Asia, with significant exposure to Malaysia's telecommunications market through its partnership with U-Mobile. Financial Performance Exceeds Expectations TeleChoice delivered FY25 results that met analyst forecasts, with revenue and profit after tax and minority interests (PATMI) reaching 105% and 103% of expectations respectively. Revenue expanded substantially by 27% year-on-year to S$276 million, primarily supported by U-Mobile 4PL services. However, adjusted PATMI grew at a more modest 20% year-on-year to S$4.4 million due to inventory provisioning impacts. Shareholders benefited from a significant dividend increase, with FY25 dividends more than tripling to 0.45 cents. Personal Communications System Drives Growth The personal communications system segment remained the company's primary growth engine, with revenue surging 42% year-on-year to S$200 million. This impressive growth was fuelled by U-Mobile's expanding subscriber base and the increasing adoption of higher-value postpaid plans requiring handset subsidies. TeleChoice strategically expanded its retail footprint by increasing outlet numbers, broadening its device portfolio, and introducing additional accessories to capture greater market share. Challenges and Outlook Despite the strong revenue performance, TeleChoice faced headwinds from higher inventory provisions. The company experienced a significant spike in inventory write-downs, with provisions increasing by S$2.5 million to S$3.8 million. This provisioning was attributed to a S$11 million year-on-year rise in inventory levels during FY25, compared to S$9.3 million in FY24. Research Recommendation and Valuation Phillip Securities Research maintains its BUY recommendation on TeleChoice International, raising the target price to S$0.275 from the previous S$0.215. The firm increased its FY26e PATMI forecast by 13% to S$8.3 million. The valuation is based on a 15x price-to-earnings multiple for FY26e, benchmarked against SGX-listed companies in the system integration and software sectors. The research house noted that growth momentum in PCS remains intact, with network engineering showing signs of recovery through managed services and network buildout projects in Indonesia and Malaysia. Additionally, TeleChoice is evaluating expansion opportunities into higher-growth digital infrastructure segments, including data centres. Frequently Asked Questions Q: What were TeleChoice's key financial results for FY25? A: TeleChoice achieved revenue of S$276 million, representing 27% year-on-year growth, and adjusted PATMI of S$4.4 million, up 20% year-on-year. Results were within expectations at 105% and 103% of forecasts respectively. Q: Which business segment drove the strongest growth? A: The personal communications system (PCS) segment was the key growth driver, with revenue jumping 42% year-on-year to S$200 million, supported by U-Mobile subscriber growth and higher postpaid plans. Q: What challenges did the company face during FY25? A: TeleChoice experienced higher inventory provisions, with write-downs increasing by S$2.5 million to S$3.8 million due to a S$11 million year-on-year rise in inventory levels. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY recommendation with a raised target price of S$0.275, up from the previous S$0.215, based on 15x P/E for FY26e. Q: How did dividends perform in FY25? A: FY25 dividends more than tripled to 0.45 cents, representing a 260% increase from the previous year's 0.125 cents. Q: What expansion opportunities is TeleChoice considering? A: The company announced it is evaluating expansion into higher-growth segments within digital infrastructure, including data centres, whilst network engineering is recovering through managed services and projects in Indonesia and Malaysia. Q: What factors contributed to the PCS segment's strong performance? A: Growth was driven by U-Mobile 5G subscribers, additional retail stores, postpaid handset subsidies, a widening range of devices, and expanded accessories offerings. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Singapore Banking Sector Faces Mixed Outlook as Rates Stabilise

Interest Rate Environment Shows Signs of Stabilisation Singapore's banking sector is navigating a transitional period as interest rate declines begin to moderate. Feb's 3-month Singapore Overnight Rate Average (3M-SORA) fell by just 2 basis points month-on-month to 1.16%, marking the smallest monthly decline in 20 months. Year-on-year, the rate decreased by 168 basis points, representing the smallest annual decline in eight months. This deceleration suggests that the sharp downward pressure on interest rates may be easing. The moderation in rate declines comes as Singapore continues to attract capital inflows, with foreign exchange reserves rising 10% year-on-year in Feb 2026, reinforcing the city-state's position as a regional safe haven. Meanwhile, Hong Kong's 3-month Hong Kong Interbank Offered Rate (3M-HIBOR) declined 18 basis points month-on-month to 2.69% in Feb, continuing its fourth consecutive month of decreases. Banking Performance Reflects Sector Headwinds Singapore's major banks reported fourth-quarter 2025 earnings that fell slightly below market expectations, with overall earnings declining 5% year-on-year. This performance was primarily driven by a 5% decrease in net interest income as net interest margins compressed by 22 basis points year-on-year. However, robust fee income growth of 13% helped partially offset the decline in traditional lending income. The banking sector has shown resilience through improved deposit dynamics. Current Account and Savings Account (CASA) balances rose 12% year-on-year, whilst the CASA ratio to total deposits increased to 19.8% in Dec 2025 from 19.6% previously. This improvement in low-cost funding provides banks with a cushion against margin compression and helps lower overall funding costs. Outlook and Investment Stance Phillip Securities Research maintains a NEUTRAL stance on the Singapore banking sector, acknowledging both challenges and opportunities ahead. The research house expects fiscal year 2026 profit after tax and minority interests to increase by 7% year-on-year, supported by continued fee income growth despite ongoing pressure on net interest income. Banks are providing guidance for low to mid-single digit loan growth, with Singapore loan growth continuing to climb at 6.1% as of Jan 2026. Management teams across the sector indicate that net interest margin compression should begin to ease in fiscal year 2026 as deposit rate cuts flow through and interest rates stabilise. The research highlights that increased market volatility and higher Singapore Dollar Average Volume are boosting capital markets and fee income, helping to offset traditional banking headwinds. Additionally, rising oil prices present inflation risks that could potentially delay further rate cuts, providing some support for margins. Despite asset quality concerns at United Overseas Bank, analysts view the bank's pre-emptive provisioning approach as prudent, with overall sector risks considered contained. All three major Singapore banks have committed to completing their previously announced capital return programmes, whilst dividend yields remain attractive at 5.1% with ongoing share buybacks improving return on equity. Frequently Asked Questions Q: How did Singapore banks perform in the fourth quarter of 2025? A: Fourth-quarter 2025 bank earnings were slightly below expectations, with earnings declining 5% year-on-year primarily due to lower net interest income, though this was partially offset by 13% growth in fee income. Q: What is the outlook for net interest margins in 2026? A: Banks are guiding that net interest margin compression should ease in fiscal year 2026 as deposit rate cuts begin to flow through and interest rates stabilise, following a 22 basis point year-on-year decline in the fourth quarter. Q: How are deposit trends supporting the banks? A: CASA balances rose 12% year-on-year with the CASA ratio to deposits improving to 19.8%, providing a tailwind for banks by lowering funding costs and cushioning net interest margin compression. Q: What factors could support banking margins going forward? A: Rising oil prices raise inflation risks that could potentially delay further rate cuts, whilst increased market volatility is boosting capital markets and fee income to help offset traditional banking headwinds. Q: What is the expected profit growth for Singapore banks in 2026? A: Phillip Securities Research expects fiscal year 2026 profit after tax and minority interests to increase by 7% year-on-year, as fee income growth will be partially offset by declining net interest income. Q: What are the key risks facing the banking sector? A: The main challenges include continued net interest margin compression from declining interest rates and asset quality concerns, though overall risks are viewed as contained with banks taking prudent provisioning approaches. Q: How attractive are Singapore bank dividends currently? A: Banks' dividend yields remain attractive at 5.1%, with all three major banks committed to completing their previously announced capital return plans and ongoing share buybacks improving return on equity. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Oiltek International Shows Resilient Performance Amid Order Book Challenges

Company Overview Oiltek International Ltd operates as an engineering, procurement, construction and commissioning (EPCC) contractor specialising in oil refining and renewable energy projects. The company maintains an asset-light business model with strong return on equity metrics, positioning itself as a key player in the sustainable aviation fuel and biodiesel sectors. Financial Performance and Dividend Growth The company delivered solid financial results for FY25, with adjusted profit after tax and minority interest (PATMI) reaching 101% of forecasted expectations. Whilst revenue fell short at 83% of projections, Oiltek demonstrated strong operational efficiency through improved gross margins, which climbed to 32.8% in the second half of FY25. This margin expansion reflected the proprietary nature of projects, procurement savings, and successful project completions, maintaining strength despite a stronger ringgit. The company rewarded shareholders with a 33% increase in dividend per share to 1.2 cents. Market Challenges and Strategic Positioning New orders secured during FY25 totalled RM152 million, representing a decline from the previous year's RM207 million. This softening was attributed to changes in Indonesian palm oil policies and the company's strategic pivot towards recurrent income projects. The order book decreased by 12% year-on-year to RM312.8 million from RM354.9 million, though February announcements of RM37.2 million in new contracts helped rebuild the order book to RM350 million. Growth Prospects and Market Opportunities The sustainable aviation fuel market presents significant growth opportunities, with global demand expected to surge from 1.9 million tonnes in 2025 to 7.8 million tonnes by 2030. Recent oil price increases and the drive for energy self-sufficiency are anticipated to accelerate demand for both sustainable aviation fuel and biodiesel. Oiltek is well-positioned to capitalise on these trends through EPCC contracts, ownership stakes in sustainable aviation fuel plants, and contracts in refinery and biodiesel facilities. Investment Outlook Phillip Securities Research maintains its target price of S$1.18, valuing Oiltek at 35 times FY26 price-to-earnings ratio—a premium to Malaysian listed peers reflecting the company's strong earnings growth profile. The firm expects a significant rebound in orders for FY26, driven by both refining and renewable energy projects. With a RM100 million net cash position and 35% return on equity, Oiltek maintains financial flexibility whilst operating an efficient asset-light model. Frequently Asked Questions Q: What was Oiltek's financial performance in FY25? A: Oiltek's FY25 adjusted PATMI was within expectations at 101% of forecast, though revenue was below expectations at 83% of projections. The company increased its dividend per share by 33% to 1.2 cents. Q: How did Oiltek's gross margins perform? A: Gross margins improved significantly, climbing to 32.8% in 2H25, up from 27.4% previously. This 5.4 percentage point increase was driven by procurement savings, project completions, and the proprietary nature of projects. Q: What caused the decline in new orders? A: New orders fell to RM152 million in FY25 from RM207 million in FY24, primarily due to changes in Indonesian palm oil policies and the company's strategic pivot towards recurrent income projects. Q: What is the current status of Oiltek's order book? A: The order book declined 12% year-on-year to RM312.8 million, but recovered to RM350 million in February 2026 following the announcement of RM37.2 million in new contracts. Q: What growth opportunities does Oiltek face? A: The company is positioned to benefit from surging sustainable aviation fuel demand, expected to grow from 1.9 million tonnes in 2025 to 7.8 million tonnes by 2030, alongside opportunities in biodiesel and refinery projects. Q: What is Phillip Securities Research's recommendation? A: The research house maintains a target price of S$1.18, valuing Oiltek at 35 times FY26 PE ratio—a premium to Malaysian peers due to strong earnings growth prospects. Q: What are Oiltek's key financial strengths? A: The company maintains an asset-light business model with a 35% return on equity and holds RM100 million in net cash, providing financial flexibility for future growth opportunities. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Geo Energy Resources Poised for Strong Growth Despite Tax Rate Challenges

Company Overview Geo Energy Resources Ltd is a coal mining company operating in Indonesia, with multiple mining assets including PT Tanah Bumbu Resources (TBR), PT Triaryani (TRA), and PT Sungai Danau Jaya (SDJ) mines. The company is focused on expanding its production capacity and developing new infrastructure to support its growth ambitions. Mixed FY25 Performance Results Geo Energy Resources delivered mixed results for FY25, with revenue performance exceeding expectations whilst earnings fell short of forecasts. The company achieved FY25 revenue and profit after tax and minority interests (PATMI) of 113% and 70% of Phillip Securities Research's FY25 estimates respectively. However, earnings were significantly impacted by an unexpected surge in the effective tax rate. Tax Rate Challenges Impact Profitability The most significant headwind facing Geo Energy was a dramatic increase in its effective tax rate, which spiked to 63% compared to the estimated 22%. This substantial deviation occurred due to Indonesian authorities changing the basis for taxable income calculations. The new methodology uses the domestic Harga Patokan Batubara (HPB) coal price rather than Geo's actual export prices. The HPB price was unusually elevated during June-July, creating a much larger gap than the typical US$1-2 difference, thereby significantly increasing the company's tax burden. Strong Production Growth and Infrastructure Development Despite the tax challenges, Geo Energy demonstrated robust operational performance. Coal production in the second half of FY25 jumped 20% year-on-year to 5.9 million tonnes. This increase was primarily driven by stronger output from the TBR mine, which contributed an additional 1.1 million tonnes, and TRA mine, which added 0.4 million tonnes. However, SDJ mine production declined by 0.5 million tonnes to 0.3 million tonnes and is expected to cease production in 2026. The company is making significant progress on its major infrastructure project - a 92-kilometre hauling road and jetty costing US$190 million. This critical infrastructure is currently 80% complete and will undergo testing and commissioning from April 2026, with commercial usage planned for August-September. Phillip Securities Research models that 2.5 million tonnes of coal will be shipped through this new infrastructure in the fourth quarter of 2026. Analyst Outlook and Recommendations Phillip Securities Research maintains its BUY recommendation for Geo Energy Resources and has raised its DCF target price to S$0.75 from the previous S$0.59. This price increase reflects a reduction in the infrastructure discount from 60% to 50%. The research house maintains its FY26 earnings estimates and identifies what it calls a "trifecta boost" in earnings potential from recovering coal prices, doubled coal production capacity, and new fee income from road usage and transportation services. The analysts forecast production to remain stable at 12 million tonnes in FY26, before spiking significantly to 20 million tonnes in FY27. Supporting this optimistic outlook, coal prices are showing signs of recovery, moving from the US$40s to the US$50s range. Frequently Asked Questions Q: What was Geo Energy's FY25 financial performance compared to expectations? A: FY25 revenue exceeded expectations at 113% of forecasts, but earnings disappointed at only 70% of estimates due to a significant increase in the effective tax rate from an estimated 22% to 63%. Q: Why did the effective tax rate increase so dramatically? A: Indonesian authorities changed the taxable income computation method, using the domestic Harga Patokan Batubara (HPB) coal price rather than Geo Energy's actual export prices. The HPB price was unusually high during June-July, creating a much larger tax burden than the typical US$1-2 difference. Q: How did coal production perform in 2H25? A: Coal production jumped 20% year-on-year to 5.9 million tonnes in the second half of FY25, primarily driven by increases from TBR mine (+1.1mn tonnes) and TRA mine (+0.4mn tonnes), whilst SDJ mine production fell by 0.5mn tonnes. Q: What is the status of Geo Energy's major infrastructure project? A: The 92-kilometre US$190 million hauling road and jetty is 80% complete. Testing and commissioning will begin in April 2026, with commercial usage planned for August-September 2026. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY recommendation and has raised the DCF target price to S$0.75 from the previous S$0.59, reflecting a reduction in the infrastructure discount from 60% to 50%. Q: What are the production forecasts for FY26 and FY27? A: Production is forecast to remain stable at 12 million tonnes in FY26, then spike significantly to 20 million tonnes in FY27 as the new infrastructure becomes operational. Q: How are coal prices performing? A: Coal prices are showing signs of recovery, moving from the US$40s to the US$50s range, which supports the positive outlook for the company. Q: What is the "trifecta boost" mentioned by analysts? A: The trifecta boost refers to three factors expected to drive earnings growth: rebounding coal prices, a doubling of coal production capacity, and new fee income from road usage and transportation services. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

China Aviation Oil Sees Strong Recovery with Soaring Jet Fuel Volumes and Expanding Margins

Company Overview China Aviation Oil (CAO) operates as a leading jet fuel supplier and trader, serving as a critical link in China's aviation fuel supply chain. The company's business model centres on jet fuel supply and trading activities, with significant exposure to China's aviation recovery through its associate Shanghai Pudong International Airport. Exceptional Financial Performance CAO delivered impressive results in the second half of 2025, with profit after tax and minority interests (PATMI) exceeding expectations at 55% and 77% of full-year forecasts respectively. The company demonstrated remarkable operational efficiency as gross profit surged 140% year-on-year to US$42.4 million in 2H25, despite revenue declining 1.3% to US$7.9 billion due to lower oil prices. Strong Volume Growth Drives Recovery The company's operational metrics reflect China's robust aviation recovery. Total supply and trading volumes increased 3.4% year-on-year to 12.15 million metric tonnes in 2H25, whilst jet fuel volumes rose significantly by 15.3% to 8.8 million metric tonnes. This growth was underpinned by China's passenger volume recovery, which increased 5.5% to 770 million passengers, with international route passengers surging 21.6% to 79.7 million. Shanghai Pudong International Airport (SPIA) remained a cornerstone of profitability, contributing US$31.9 million in 2H25 profits—44.6% higher year-on-year and representing 52.6% of total PATMI. Key Positives Driving Performance The margin expansion story reflects two critical factors: enhanced negotiating power from higher jet fuel volumes enabling better spread negotiations and improved fixed cost absorption across a larger supply base. Additionally, potential increases in sustainable aviation fuel (SAF) volumes, which carry margins three to five times higher than conventional jet fuel, contributed to profitability improvements. CAO maintains a fortress balance sheet with US$686.9 million in cash and no debt, providing strategic flexibility for dividend increases and investments. Research Outlook Phillip Securities Research maintains a BUY rating with an upgraded target price of S$2.53, previously S$1.50. The research house increased FY26 PATMI forecasts by 32% to account for continued air travel recovery and SPIA's Terminal 3 expansion, which will increase passenger handling capacity by approximately 62.5%. Frequently Asked Questions Q: What drove CAO's strong financial performance in 2H25? A: Jet fuel volumes increased 15.3% year-on-year to 8.8 million metric tonnes, whilst gross profit surged 140% to US$42.4 million due to margin expansion and higher refuelling volumes supported by China's passenger volume recovery. Q: How significant is Shanghai Pudong International Airport to CAO's profitability? A: SPIA contributed US$31.9 million in 2H25 profits, representing 44.6% higher year-on-year growth and accounting for 52.6% of CAO's total PATMI in the period. Q: What is Phillip Securities Research's recommendation and target price? A: Phillip Securities Research maintains a BUY rating with an upgraded target price of S$2.53, increased from the previous S$1.50, representing a 32% increase in FY26 PATMI forecasts. Q: Why did margins expand despite lower oil prices? A: Margin expansion resulted from higher jet fuel volumes enabling better spread negotiation and fixed cost absorption, plus potential increases in sustainable aviation fuel volumes, which carry margins three to five times higher than conventional jet fuel. Q: What is CAO's financial position? A: CAO maintains a strong net cash position of US$686.9 million with no debt, providing flexibility for dividend increases and strategic investments. Cash balance grew US$186.7 million in FY25 due to strong operating cash flows of US$150.5 million. Q: What growth drivers support the upgraded forecasts? A: Growth will arise from higher passenger volumes following SPIA's Terminal 3 expansion, which increases passenger handling capacity by approximately 62.5%, and strategic investments supporting the growing SAF business. Q: How did passenger recovery impact CAO's operations?? A: China's passenger volumes increased 5.5% to 770 million, with international route passengers surging 21.6% to 79.7 million, directly supporting the 15.3% increase in jet fuel volumes. Q: What role does sustainable aviation fuel play in CAO's strategy? A: SAF volumes are expected to grow alongside international travel recovery and carry margins three to five times better than conventional jet fuel, contributing to the company's profitability expansion. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Centurion Corporation Positioned for Fee Income Growth Despite Mixed Results

Company Overview Centurion Corporation Ltd operates purpose-built worker accommodation (PBWA) and purpose-built student accommodation (PBSA) across Singapore, Malaysia, the UK, and Australia. The company has recently spun off its real estate investment trust, CAREIT, positioning itself to benefit from scalable property management fee income. Financial Performance Highlights Centurion delivered mixed results in 2H25, with revenue exceeding expectations at 105% of full-year forecasts, reaching S$155.2 million. This strong revenue performance was primarily driven by the consolidation of the remaining 55% stake in the 6,290-bed Westlite Mandai facility, which represents 17% of Singapore's bed capacity. However, adjusted profit after tax and minority interests (PATMI) fell short of expectations at 91% of forecasts, impacted by a 33% year-on-year increase in administrative fees due to higher manpower costs. Key Positive Developments Singapore PBWA operations demonstrated robust growth, with 2H25 revenue increasing 24% year-on-year to S$113 million. Beyond the Westlite Mandai consolidation, positive rental revisions contributed to this growth. The newly operational 1,650-bed Westlite Ubi facility, featuring rental rates estimated to be 5-10% higher than existing properties, further supported Singapore revenue expansion. The company's balance sheet has strengthened significantly following CAREIT's spin-off, generating approximately S$473 million in net proceeds. Net debt decreased 38% year-on-year to S$332 million, whilst the net gearing ratio improved substantially to 27% from 46% in FY24. CAREIT's property management fees present a promising revenue stream, with Centurion recognising S$6.5 million in revenue and S$3.2 million in PATMI during 4Q25, achieving a healthy 49% profit margin. Analysts estimate CAREIT's revenue will grow 25% year-on-year in FY26, potentially generating approximately S$16 million in property management fees for Centurion. Challenges Australia PBSA operations faced headwinds, with revenue declining 7.6% year-on-year to S$9 million. Occupancy rates dropped to 93% from 96% in FY24, primarily due to student arrival delays caused by visa requirement changes. However, the Australian government's decision to raise the student visa cap by 9% to 295,000 in August 2025 suggests potential recovery ahead. Investment Outlook Phillip Securities Research maintains a BUY recommendation with an unchanged target price of S$1.81. The firm expects FY26 consolidated adjusted PATMI to decline approximately 14% year-on-year due to increased profit attributable to minority interests from CAREIT's inclusion. Centurion has proposed a special dividend-in-specie distribution of one CAREIT unit for every ten Centurion shares, estimated to yield shareholders approximately 7%. Frequently Asked Questions Q: What drove Centurion's strong revenue performance in 2H25? A: Revenue exceeded expectations primarily due to the consolidation of the remaining 55% stake in the 6,290-bed Westlite Mandai facility and positive rental revisions across the Singapore PBWA portfolio. Q: Why did adjusted PATMI fall below expectations despite strong revenue? A: Adjusted PATMI was impacted by a 33% year-on-year increase in administrative fees, excluding CAREIT IPO fees, primarily due to higher manpower costs. Q: How significant is the CAREIT property management fee income? A: In 4Q25, Centurion recognised S$6.5 million in revenue and S$3.2 million in PATMI from CAREIT property management fees, with a healthy 49% profit margin. This income stream is estimated to grow 25% year-on-year in FY26. Q: What challenges did the Australia PBSA segment face? A: Australia PBSA revenue declined 7.6% year-on-year due to occupancy dropping to 93% from 96%, caused by delays in student arrivals due to visa requirement changes. Q: How has Centurion's balance sheet improved? A: Following CAREIT's spin-off, net debt decreased 38% year-on-year to S$332 million, and the net gearing ratio improved to 27% from 46% in FY24, benefiting from approximately S$473 million in net proceeds. Q: What is Phillip Securities Research's recommendation? A: Phillip Securities Research maintains a BUY recommendation with an unchanged target price of S$1.81, before the dividend-in-specie distribution. Q: What special dividend is Centurion proposing? A: Centurion has proposed a special dividend-in-specie distribution of one CAREIT unit for every ten Centurion shares, estimated to yield shareholders approximately 7%. Q: What is the outlook for Australia PBSA operations? A: The Australian government raised the student visa cap by 9% to 295,000 in August 2025, which is expected to improve Australia PBSA occupancy in FY26 through increased international student demand. This article has been auto-generated using PhillipGPT. It is based on a report by a Phillip Securities Research analyst. Disclaimer These commentaries are intended for general circulation and do not have regard to the specific investment objectives, financial situation and particular needs of any person. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any person acting based on this information. You should seek advice from a financial adviser regarding the suitability of any investment product(s) mentioned herein, taking into account your specific investment objectives, financial situation or particular needs, before making a commitment to invest in such products. Opinions expressed in these commentaries are subject to change without notice. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of units in any fund and the income from them may fall as well as rise. Past performance figures as well as any projection or forecast used in these commentaries are not necessarily indicative of future or likely performance. Phillip Securities Pte Ltd (PSPL), its directors, connected persons or employees may from time to time have an interest in the financial instruments mentioned in these commentaries. The information contained in these commentaries has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in these commentaries are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in these commentaries are subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages. The companies and their employees mentioned in these commentaries cannot be held liable for any errors, inaccuracies and/or omissions howsoever caused. Any opinion or advice herein is made on a general basis and is subject to change without notice. The information provided in these commentaries may contain optimistic statements regarding future events or future financial performance of countries, markets or companies. You must make your own financial assessment of the relevance, accuracy and adequacy of the information provided in these commentaries. Views and any strategies described in these commentaries may not be suitable for all investors. Opinions expressed herein may differ from the opinions expressed by other units of PSPL or its connected persons and associates. Any reference to or discussion of investment products or commodities in these commentaries is purely for illustrative purposes only and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products or commodities mentioned. This advertisement has not been reviewed by the Monetary Authority of Singapore.

17LIVE Group Limited Maintains BUY Rating Despite Revenue Decline